How Long Does Workers' Comp Last in Florida? How Long Does It Take to Get Workers' Comp Checks?

If you or an employee has been injured in a workplace accident, you might be wondering how to get workers’ comp in Florida and how long the process will take. Understanding these timelines is crucial to ensure you receive the benefits you’re entitled to under Florida law.

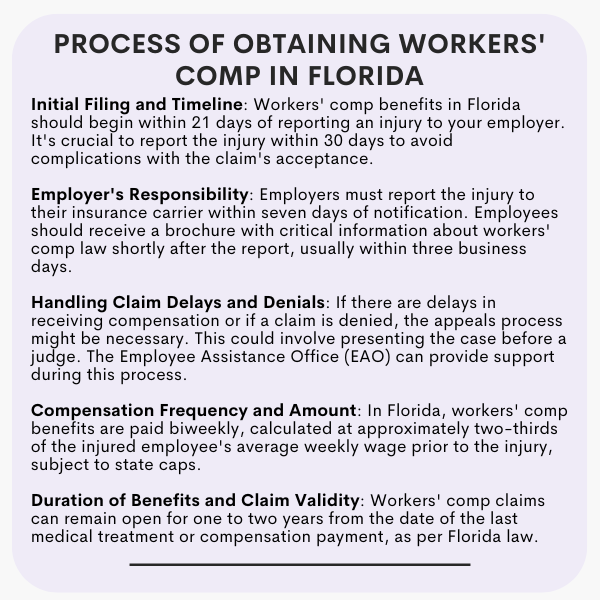

In Florida, workers’ comp benefits aim to provide timely support for injured workers. After reporting an injury to your employer, you can expect the first workers’ comp check to arrive within 21 days, provided the claim is approved. This relatively quick turnaround helps injured employees focus on recovery rather than financial stress.

The length of time workers’ comp benefits last in Florida depends on the nature and severity of the injury. Temporary benefits can last up to 104 weeks, while permanent benefits may continue for much longer, depending on the circumstances.

How to Get Workers’ Comp in Florida

The process starts with promptly reporting the injury to your employer. To improve your chances of a smooth claims process, it’s essential to file the claim within 30 days of the incident. Delays can complicate approval and may reduce your likelihood of receiving benefits.

Workers’ comp in Florida is designed to assist injured workers in covering medical bills and lost wages. By following the proper steps and adhering to timelines, you can ensure the process goes as smoothly as possible.

When Should You File a Workers' Compensation Claim?

To maximize your chances of a successful claim, report any workplace injury immediately and file your claim as soon as possible. Florida law requires claims to be reported within 30 days of the injury. Waiting too long can jeopardize your ability to receive benefits.

Should My Employer Report My Claim?

After an injury on the job, your employer should promptly report it to their insurance carrier within seven days of becoming aware.

Along with this notification comes a brochure outlining key information about workers' compensation law that you need to be aware of – and fast! The insurer must send out the materials right away, usually arriving in three business days or less.

For deeper insight into system specifics and procedures, check-out the “Brochures” section on the Myfloridacfo.com website, where the same informational packet can also be found.

Filing A Workers Comp Claim

Although fast claims processing times are possible, don't be surprised if your insurance company pays its due diligence in reviewing and denying the claim. Be ready for unexpected delays to ensure you get the coverage you deserve!

If a workers’ comp payment is delayed, the appeals process may need to be initiated. Unfortunately, this could mean having to take matters into your own hands and presenting your case before a judge in order for it to be resolved quickly.

What If My Employer Does Not Report My Injury?

You have the right to report a workplace injury in Florida, as per Section 440.185 of the state statutes.

If you require help with this process however, please don’t hesitate to contact the Employee Assistance Office (EAO). They can be reached by phone at 800-342-1741 or via email at wceao@myfloridacfo.com – get back on your feet and protect yourself today!

What If My Workers Compensation Claim Is Denied?

When facing a dispute, it's important to be aware of the assistance that is available.

The Employment Assistance Office (EAO) provides no-cost services, including helping you attempt to resolve your issue and filing petitions for benefits when needed – all without hiring an attorney.

For further information, contact us at (800) 342-1741 or by e-mailing wceao@myfloridacfo.com; we also have District Offices located throughout Florida as well!

How Often Does Workers Compensation Pay?

In Florida, workers comp benefits are tailored to fit the individual. After an on-the-job injury or illness, benefit checks arrive biweekly and provide financial relief based off each person's average weekly wage.

If you were injured on the job, your benefit check could be up to two-thirds of what you made during a three month period just before that injury – as long as it doesn’t exceed state limits. This money is often paid out in bi-weekly installments.

Will I Be Paid If I Lose Time From Work?

Are you facing a disability in Florida?

Be aware that according to state law, benefits are not paid out for the initial seven days of disablement. However, if your condition remains longer than three weeks and continues into day eight or beyond, then insurance may provide payment for those first few days.

How Long Does My Workers Comp Claim Remain Open?v

How Long Does My Workers Comp Claim Remain Open?

Depending on when the injury occurred, this could be either one or two years from either your last medical treatment or payment of compensation – as outlined by Section 440.19(2) in Florida State Law. Don’t miss out!

What is Pay As You Go Workers Comp?

Pay As You Go Workers Comp is an innovative insurance coverage solution that enables businesses to reduce the cost of providing workers compensation coverage while remaining compliant with state and federal laws.

It provides short-term workers comp coverage for any company, giving them the flexibility to meet their needs in a timely manner. With this option, companies are able to cover their employees at a fraction of the cost associated with traditional policies.

In addition, Pay As You Go Workers Comp allows employers to keep track of their employees’ claims and payments, allowing them to stay on top of any potential risks or liabilities.

This type of insurance can also be beneficial for companies who are subject to changing needs due to seasonal fluctuations or other unexpected changes in demand.

By taking advantage of Pay As You Go Workers Comp, businesses can ensure they’re always covered while keeping costs low.

How Does Pay As You Go Workers Comp Work?

Pay as you go workers comp is a great way for businesses to manage their workers compensation liabilities and costs.

OCMI can help with this, by providing coverage through the state’s workers comp program with real-time payments that are calculated and made throughout the year.

This type of plan allows employers to easily budget their workers comp payments and eliminates large end-of-year bills that can be difficult to manage. By working with OCMI, employers can pay premiums in fixed monthly or quarterly installments based on their current payroll and estimated future payroll amounts.

The company will then adjust the premium payments as necessary for any changes in payroll numbers, so employers are always paying the appropriate amount for their coverage needs.

Additionally, OCMI also offers access to an online portal that makes managing policies and reporting claims easier than ever before. With this kind of convenience, plus the flexibility of pay as you go workers comp plans, it’s no wonder why more businesses are turning to OCMI for their coverage needs!

How can Pay As You Go Workers Comp help businesses save money on workers compensation insurance premiums?

Pay As You Go Workers Comp is an innovative way for businesses to save money on their workers compensation insurance premiums.

By utilizing this system, businesses can pay for the exact amount of coverage they need as they go – rather than having to pre-pay for the year in one lump sum. This means that if a company’s payroll changes throughout the year, their premium payments will adjust accordingly. Additionally, because the premium is based on actual payroll, employers will not have to pay more than what’s required and can rest assured that they are paying a fair rate.

Pay As You Go Workers Comp also allows businesses to make payments via ACH or credit cards with no additional processing fees.

Overall, Pay As You Go Workers Comp offers significant financial benefits over traditional workers compensation insurance plans and provides employers with peace of mind knowing that they are only paying what’s necessary to provide adequate coverage for their employees.

What Are The Benefits of Using Pay As You Go Workers Comp for Businesses?

Pay As You Go Workers Comp is an incredibly beneficial option for businesses large and small.

It allows businesses to pay their workers comp premium on an ongoing basis, as it accrues, relieving them of the burden of a lump sum payment.

This means that businesses can budget more effectively, avoiding the financial strain of needing to cover an unexpected bill for their workers comp premiums. Additionally, this type of system offers businesses greater flexibility in terms of how much they need to pay each month.

With Pay As You Go Workers Comp, businesses only have to pay for what they are using at any given time and can adjust their payments easily when needed.

Furthermore, because workers comp premiums are based on current wages rather than the total payroll number, businesses can save money by taking advantage of lower commissions when their employees’ salaries increase.

Finally, Pay As You Go Workers Comp helps create a safer workplace by ensuring that employers are up-to-date with their workers compensation insurance coverage and helping employers make sure that all safety regulations are met.

How Can Businesses Get Started With Pay As You Go Workers Comp?

Businesses can get started with Pay As You Go Workers Comp by consulting a OCMI Workers Comp to find out what their options are.

To get started, businesses should research the best-rated providers and compare their coverage plans, pricing structure, and customer service reviews.

Businesses should also investigate how much coverage they need for each employee and any additional benefits that may be offered with the plan.

Employers should also consider the convenience of setting up automatic payments through the provider to make sure their premiums are paid on time each month.

Ultimately, Pay As You Go Workers Comp provides businesses with an affordable way to stay compliant with workers compensation regulations and protect employees in case of injury or illness while on the job.

Are there any drawbacks to using Pay As You Go Workers Comp?

One of the primary drawbacks to using Pay As You Go Workers Comp is that it can be expensive.

This is due to the fact that employers are required to pay for workers comp coverage on a regular basis and cannot take advantage of lower premiums that may be available if they were able to pay for an annual policy in advance.

Additionally, some employers may not have the cash flow necessary to sustain regular payments and may be unable to afford a comprehensive workers comp policy.

Lastly, not all states allow Pay As You Go Workers Comp, so employers in those states will have no choice but to obtain traditional annual policies or risk getting fined or having their business shut down.

Now that you know all about Pay As You Go Workers Comp, does it sound like something your business could benefit from? If you’re interested in learning more about how OCMI can get you the best workers comp rates, give us a call or fill out our online form to request a quote.

We’d be happy to answer any questions you have and help you get started with this cost-saving solution for your business.

Top Nine Workers Comp Questions

As a business owner, it is important to be aware of the legal risks associated with workers’ compensation. Knowing the answers to the top nine workers comp questions can help protect your business and employees.

What is Workers Comp?

Workers’ compensation serves as an essential safety net for both employers and employees when workplace injuries occur, and understanding the key components of this system is critical.

Here are some of the most frequently asked questions regarding workers’ compensation:

By understanding the answers to these common questions, you can ensure that you are making informed decisions about protecting your business and your employees from financial losses due to workplace accidents.

What Types of Injuries Are Covered by Workers' Compensation?

Workers' compensation covers a wide range of workplace injuries, both physical and psychological. Injuries that are covered include those that are the direct result of an accident or a specific event such as a fall or being struck by an object.

It may also cover repetitive motion injuries caused by long-term repetitive motions such as typing or lifting objects. Additionally, some illnesses may be covered if they can be directly linked to the conditions of your job, such as those caused by exposure to hazardous materials or poor air quality in the workplace.

Mental health issues associated with work-related stressors may also be included in coverage.

For physical injuries, workers’ compensation typically covers medical bills for treatments related to the injury, lost wages due to time off work while recovering, and any necessary rehabilitation costs such as physical therapy.

If the injury leads to permanent disability, coverage may also extend to vocational rehabilitation services and/or payments for any long-term loss of earnings capacity due to the injury. For psychological injuries such as PTSD or depression, coverage typically includes mental health treatment from a professional therapist and medications if prescribed by a physician.

In some cases, workers’ compensation may even cover home modifications needed for someone with a physical disability related to their injury.

When Must an Employer Provide Notice of a Workplace Injury?

Workplace injuries are a common and unfortunate reality of most work environments.

As an employer, it is important to be aware of the legal requirements for providing notice when an employee has suffered an injury on the job.

Generally, employers must provide notice of a workplace injury as soon as practicable after becoming aware of it. In many countries and states, employers may need to report any workplace injuries that require medical attention or results in lost time from work within a certain timeframe.

Depending on the severity of the injury, employers may also be required to take certain other steps including filing reports with federal or state agencies or making worker’s compensation claims.

In addition to having knowledge of these reporting requirements, employers should ensure employees are familiar with their rights in the case of a workplace injury and with the procedures for reporting an incident.

Employers should inform employees about who they should speak to about their injury and what documentation will be necessary for any paperwork related to filing claims or seeking medical attention.

It is also important for employers to have policies in place regarding how workplace injuries will be handled so that all parties involved have clear expectations regarding their responsibilities and liabilities during this difficult time.

Is There a Time Limit on Filing a Claim?

Workplace injuries are a common and unfortunate reality of most work environments. As an employer, it is important to be aware of the legal requirements for providing notice when an employee has suffered an injury on the job.

Generally, employers must provide notice of a workplace injury as soon as practicable after becoming aware of it. In many countries and states, employers may need to report any workplace injuries that require medical attention or results in lost time from work within a certain timeframe.

Depending on the severity of the injury, employers may also be required to take certain other steps including filing reports with federal or state agencies or making worker’s compensation claims.

In addition to having knowledge of these reporting requirements, employers should ensure employees are familiar with their rights in the case of a workplace injury and with the procedures for reporting an incident.

Employers should inform employees about who they should speak to about their injury and what documentation will be necessary for any paperwork related to filing claims or seeking medical attention.

It is also important for employers to have policies in place regarding how workplace injuries will be handled so that all parties involved have clear expectations regarding their responsibilities and liabilities during this difficult time.

How Much Money is Paid Out in Benefits?

Workers compensation benefits, or workman's compensation, are payments made to employees who become injured while on the job.

The amount of money paid out in workers comp benefits varies depending on the type and severity of the injury or illness.

Each state has its own laws that dictate how much an employee can receive in these benefits, but generally speaking, most states provide at least a portion of lost wages and medical expenses for workers with disabilities caused by workplace injuries.

In 2019, the U.S. Bureau of Labor Statistics estimated that workers comp benefits totaled nearly $75 billion in payments and covered close to 8 million claims.

Of this total, nearly $59 billion was spent on wage replacement benefits, with more than $15 billion going towards medical treatment and other costs associated with workplace injuries.

This number is likely to increase as awareness about workplace safety increases and more employers take steps to protect their employees from accidents or illnesses incurred on the job. In addition to providing monetary aid for injured employees, workers comp also helps employers avoid costly litigation fees associated with lawsuits stemming from unsafe work environments.

How Long Do Benefits Last?

Workers’ compensation benefits can last for varying lengths of time, depending on the severity of the injury and its effects.

In most cases, workers’ comp benefits will last until the worker has recovered from their injury and is able to return to their job.

This timeframe can range from weeks to months or even years in more serious cases. If the worker cannot ever fully recover due to a disability, they may be eligible for additional long-term benefits.

When an employee has been injured on the job, they are entitled to a range of medical expenses and wage replacement benefits through workers’ compensation insurance.

These include money for immediate medical care, ongoing medical treatments and physical therapy if necessary, as well as a portion of income while the worker is unable to work.

Depending on the laws in their state, workers may also be eligible for death benefits if a loved one dies as a result of a workplace injury or illness.

The length of these benefits depends on the nature and severity of the injury or illness; some states have maximum lengths for different types of injuries that cannot exceed certain periods of time. For example, many states cap off payments after 400 weeks for permanent disability due to an injury or illness.

Who Pays For Medical Care Related to Workplace Injuries?

Workplace injuries can be devastating and costly, not only in terms of physical and emotional suffering but also financially.

Depending on the severity of the injury, medical care related to a workplace injury may include surgery, medication, rehabilitation, physical therapy or other treatments.

The party responsible for paying for these healthcare costs will vary depending on the circumstances of the injury and the state in which it occurs.

In most cases, employer-provided workers’ compensation coverage pays for medical bills related to a workplace injury.

This coverage is typically provided by the employer’s insurance company; however, some states may have their own workers’ compensation funds that employers must pay into in order to provide coverage. In addition to covering medical expenses related to an employee’s workplace injury, workers’ compensation also covers lost wages while they are recovering from the injury.

In some jurisdictions, an employee may be able to sue their employer if they feel that an inadequate amount was paid out by workers’ compensation. However, this is typically only an option in cases where there was gross negligence or intentional harm on behalf of the employer.

Is There Any Protection Against Potential Litigation When it Comes to Workers’ Comp Cases?

When it comes to workers’ comp cases, employers are required to provide protection for their employees in order to prevent potential litigation. Employers must provide the necessary insurance coverage and comply with the laws governing workers’ compensation.

This includes making sure their employees have access to the compensation they are entitled to and that all of the necessary paperwork is filed correctly. Additionally, employers must also ensure that they are taking all reasonable steps to reduce employee injuries and protect them from harm while on the job.

Employers also need to be aware of any potential legal risks that may arise due to a worker’s compensation claim. In such cases, employers should consult an attorney who specializes in workers’ compensation law in order to understand their rights and obligations under the applicable state laws.

Employers can also look into purchasing Employment Practices Liability Insurance (EPLI) which helps cover potential costs related to lawsuits resulting from employee issues such as discrimination, wrongful termination or sexual harassment.

Additionally, employers should ensure that they are implementing proper training programs and safety protocols within their workplace to minimize liability exposure from potential injury claims made by their employees.

Finally, employers should stay up-to-date on changes in federal, state or local regulations regarding workers’ compensation in order to remain compliant with applicable laws and regulations.

Can An Employee Sue Their Employer For Damages Related to Work-Related Injuries or Illnesses?

Yes, an employee can sue their employer for damages related to work-related injuries or illnesses.

In most cases, employees are covered by workers’ compensation laws which provide access to medical benefits and a portion of lost income in case of an injury or illness related to the workplace.

An employee may also be able to make a personal injury claim against their employer’s insurance in addition to workers’ compensation benefits. This type of claim is necessary when the injury or illness was due to the negligence of the employer or a third party, such as a manufacturer who supplied faulty machinery.

In some cases, an employee may be eligible for punitive damages (in addition to compensatory damages) if it is found that their employer acted with malicious intent, was grossly negligent, or otherwise knowingly endangered their employees without reasonable cause.

Punitive damages are designed to punish employers who have acted unlawfully and sought to prevent future harm from occurring.

Employees should consult with an experienced legal professional before considering any type of lawsuit against their employer as there are specific rules and statutes governing this kind of action that must be followed in order for it to be successful.

What Kind of Evidence Does an Employee Need to Prove Their Case Before The Court?

When an employee takes their case to court, they need to provide evidence to prove their claims. This evidence can take several forms, including witness statements, physical documents or objects, medical or expert witness testimony, financial records and other relevant items.

To be considered legally valid in a court of law, the evidence must generally meet certain criteria. It should be reliable and able to withstand scrutiny by the opposing party’s attorney. It should also be relevant to the claims being made and should be verifiable from multiple sources such as eyewitness accounts or written accounts from official records.

Additionally it should not have been tampered with in any way, as this could weaken its integrity. The employee should also have solid proof that they are the owner of any documents presented to the court and that these documents are authentic.

Furthermore, all witnesses who testify on behalf of the employee must be credible and able to provide testimony that is both convincing and accurate. To ensure that their case is stronger than their opponent’s case, employees should present as much evidence as possible in order for it to stand up under legal scrutiny.

Understanding workers’ compensation laws is important for employers and employees

In conclusion, understanding workers’ compensation laws is important for employers and employees alike.

Knowing the answers to the top nine workers’ comp questions will help ensure that both parties understand their rights and responsibilities regarding workplace injuries. Additionally, it can help employers create a safe work environment for their workforce and provide them with the protection they deserve in case of an unfortunate event.

Furthermore, workers’ compensation policies help protect companies from costly lawsuits that could result from injuries or illnesses sustained on the job. Understanding these benefits makes it clear why it is so important to become informed about all aspects of workers’ compensation law.

What Are Five Types of Issues That Are Not Covered by Workers Compensation?

Workers’ comp provides benefits to employees who are injured or become ill as a result of their job.

At times, life can take unexpected turns. Health issues, accidents and unforeseeable events can cause turmoil in our lives, affecting both the mind and body.

Thankfully, Workers’ Comp insurance provides a helping hand to those who require it most — offering support and safety nets for employees who have been injured due to their job or work conditions.

Have you ever wondered what’s not covered by Workers Compensation? If you’ve ever been an employee or business owner in the state of Florida, it’s important to understand the parameters of the system.

After all, if a workplace emergency arises, it’s often those workers compensation regulations that will determine whether medical costs are covered—and who is responsible for their payment!

It may surprise you to learn just which scenarios and issues don’t quite fall within its scope: In this blog post we’re exploring five key areas of trouble that isn’t included with your basic workers comp package. Let’s get started!

Workers Compensation Does Not Cover Violence

Intentional Injuries: The workplace can be a dangerous place. From slips and falls to serious injuries, accidents happen all the time.

If you engage in misconduct or recklessness that results in an injury, workers comp won’t kick in. That means your employer can’t be held accountable and medical costs are on you.

Every year, millions of American workers face the threat of violence while on the job. Though official records report 2 million victims per annum, experts believe that number is much higher given how many incidents go unreported. Those stats are taken from the Occupational Safety and Health Administration (OSHA).

Fortunately, workers compensation is there to help you out in case of an accident or injury. But what happens when the workplace hazard isn’t an accident? As it turns out, your workers comp might not cover you if you’re injured due to violence at work.

The main reason why workers comp doesn’t cover violence is because it’s considered an intentional act rather than an accidental one. For example, if someone trips over a cord and breaks their arm, they would be eligible for workers comp benefits because it was an accident.

But if someone gets into a fight with another employee and ends up getting hurt as a result, they would not be eligible for workers comp because it was not an accident – it was intentional.

Injuries caused by workplace violence can have a devastating impact on your life, yet they may not always be covered with workers’ compensation.

In order to receive the benefits you deserve if these unfortunate circumstances arise, it’s essential that victims seek professional legal help for their case.

With an experienced attorney at their side, employees who experience violent attacks in the office will get access to resources needed for proving their claim and ultimately obtaining proper coverage through workers’ comp.

Workers Comp Does Not Cover Mental Health Conditions:

As much as we’d like to think that our employers have our backs, there are exceptions to their protection. One of these exceptions is mental health.

As it stands, workers’ compensation does not cover mental illnesses or psychological distress. This means that if you suffer from a mental illness, you may be out of luck when it comes to getting coverage for your medical expenses.

While physical injuries sustained at work will usually be covered under workers comp, the same doesn’t apply for mental health issues. Mental health conditions can arise from the stress and strain of work, but these are not covered by workers comp.

The law states that an employer must provide compensation for any injury sustained on the job or due to the nature of the job itself.

This includes physical injuries and illnesses, such as carpal tunnel syndrome or a sprained ankle.

Even if the injury was due to negligence on the part of the employee, they are still eligible for coverage under workers’ compensation insurance. However, unfortunately this law does not extend to those suffering from mental illness or psychological distress caused by work-related stressors.

It’s important to note here that most states do not require employers to cover workplace-induced trauma or stress in their workers’ comp insurance plans—and that’s where things get tricky.

While physical ailments can be easily proven with medical records and reports, emotional issues are more abstract and subjective. This makes it difficult for employees who need help managing mental health issues stemming from their jobs but don’t have access to resources through workers’ comp insurance benefits.

The good news is that many employers are beginning to recognize this gap in coverage and are taking steps towards offering more comprehensive plans when it comes to employees’ mental wellbeing.

For example, some companies now offer additional counseling sessions or flexible hours so that employees can manage their emotional well-being without risking their job security or financial stability in the process.

Though there is still a long way to go before all employers provide adequate protections for those suffering from workplace-induced mental health issues, progress is being made at a steady pace.

Mental health should never be overlooked in favor of physical safety; both should always be taken into account when discussing workers’ compensation benefits and protection plans provided by employers.

It’s only by recognizing this gap and working together that we can make sure everyone has access to fair coverage regardless of what type of ailment they’re dealing with—be it physical or psychological.

Workers Compensation Does Not Cover Pre-Existing Conditions

If you have a pre-existing condition prior to beginning your job, this condition will not be covered under workers compensation. However, if your pre-existing condition is aggravated or exacerbated by the duties and tasks you must do in the course of your job, then this may be covered.

It’s important to keep track of any new health issues that arise at work, so you can make sure you are getting appropriate coverage if needed. Additionally, documenting changes in your pre-existing health condition is also important as well. This will help ensure that you get the care and coverage necessary if it is affected by your job duties.

It is always a good idea to discuss any health issues you may have with your supervisor, so that they can be aware and help support you. Additionally, contact your state’s workers compensation board for more information on what health conditions are covered.

With the right knowledge and advocacy, you can ensure that all of your health needs are taken care of. If you have any questions, don’t hesitate to speak with a healthcare professional or your supervisor. They can help provide the guidance and resources needed to ensure that you get the most appropriate coverage for your health conditions.

Workers Comp Does Not Cover Horseplay

Let's face it – when you go to work, sometimes playtime is inevitable. Whether you're trading funny stories with co-workers or engaging in a lighthearted game of "pranking for laughs," the idea of horseplay has probably entered your mind at some point.

Unfortunately, what might seem like harmless fun can cause serious injuries – so if that happens, don’t count on workers comp to foot the bill!

Remember that workers compensation does not cover any injuries or illnesses caused by horseplay.

If you are injured in an accident due to your own reckless actions or the actions of another employee, then it is highly unlikely that workers comp will cover those costs. Be sure to follow all safety protocols and take extra precautions when engaging in activities on the job site. In the event of an injury, you should report it to your supervisor immediately.

And if you witness any horseplay that could lead to injury, be sure to intervene and inform everyone involved of the potential consequences. This can help prevent serious accidents in the workplace.

At the end of the day, safety is key – so don’t let horseplay be an issue in your workplace. It’s important to take it seriously and ensure everyone stays safe on the job.

Workers Comp Does Not Cover Car accidents while driving for work purposes

Commuting to work can be hazardous for your health, but even if you get injured on the way in or out of your job, it won't count as workplace-related—unless you have special permission from higher ups!

Workers compensation does not cover car accidents that happen while driving for work purposes, even if the employee is on company time.

Be sure to talk to your employer about any specific policies in place so you are aware of how and when you may be covered by workers comp or other insurance provisions.

Protects From Lawsuits:

It helps protect employers from costly lawsuits in the event of an employee being injured while on the job. It covers medical expenses, lost wages, and other costs related to work-related injuries or illnesses.

This includes some types of accidents that occur while travel, such as slips and falls in the workplace, exposure to hazardous materials, repetitive strain injuries, and more.

Medical Expenses and Lost Wages:

Workers’ comp covers medical expenses and lost wages for employees injured on the job. This includes coverage for doctor’s visits, hospital stays, prescription drugs and surgeries. It also covers lost wages while an employee is unable to work due to their injury or illness.

Rehabilitation Services:

Workers’ comp can cover physical therapy and other rehabilitation services needed as a result of a work-related injury.

Are you an employee in Florida who has recently been fired but still think you’re entitled to some kind of compensation?

Well, believe it or not, the answer may be a resounding “yes!” According to Florida law, you may in fact be able to collect workers’ comp after being terminated – even if it doesn’t seem that likely. Read on for your guide to understanding how this all works!

In the Sunshine State, protecting workers is a top priority. While on-the-job injuries can be scary and stressful to deal with, there’s some light at the end of the tunnel – as long as you meet certain requirements!

To get your well deserved compensation for workplace accidents in Florida all that needs checking off from this list: were you actually injured while working? Did it happen when clocked in? Was HR informed about what happened ASAP? Were drugs not involved per employer regulation? Are you seeing an approved doctor by your company & did sobriety prevail during incident time?! If so then those benefits are just around corner!

Getting injured on the job can be a stressful and overwhelming experience. Not only do you have to deal with the pain and hardship of recovering from an injury, but you also have to face the possibility that you might lose your job if you are unable to work.

So, can you be fired while collecting workers’ compensation benefits? The answer may surprise you.

The short answer is no. It is illegal for an employer to terminate an employee for filing a workers’ compensation claim or for receiving benefits. However, there are some circumstances where an employer may terminate an employee who is still receiving compensation benefits.

For example, if the employee has been away from work longer than the amount of time permitted by their medical leave agreement, they may be terminated due to absenteeism or abandonment of their job duties.

In addition, if the employee is cleared by their doctor to return to work but refuses to do so, they may be terminated due to insubordination or failure to follow company policies.

Lastly, if an employee has been away from work for an extended period due to injury and their position has been permanently filled by another qualified individual during that time frame, they may be terminated due to lack of available positions within the company.

Ultimately, it is important for employees who are receiving workers’ compensation benefits to remain in communication with their employers and ensure that they are adhering to all applicable laws and regulations when it comes to returning back to work after being injured on the job.

It is also essential that employees understand their rights under the law when it comes to filing a claim or pursuing legal action against their employer should they be wrongfully terminated while collecting workers’ compensation benefits.

If I Get Fired, Do I Get Workers Compensation?

You don't have to worry about losing your workers' comp benefits if you're let go - these are there for the taking as long as your work injury happened while on their watch.

So even with a new boss in town, medical care and replacement wages will still be yours; just call our office right away if anyone tries to take them off the table!

Employees should know that the law provides protection against employers who try to punish injured workers for filing a claim or otherwise seek retribution.

If an employer fires a worker just for seeking compensation, then they are in violation of the law and could be held liable for damages.

It is important for employees to understand their rights and responsibilities when it comes

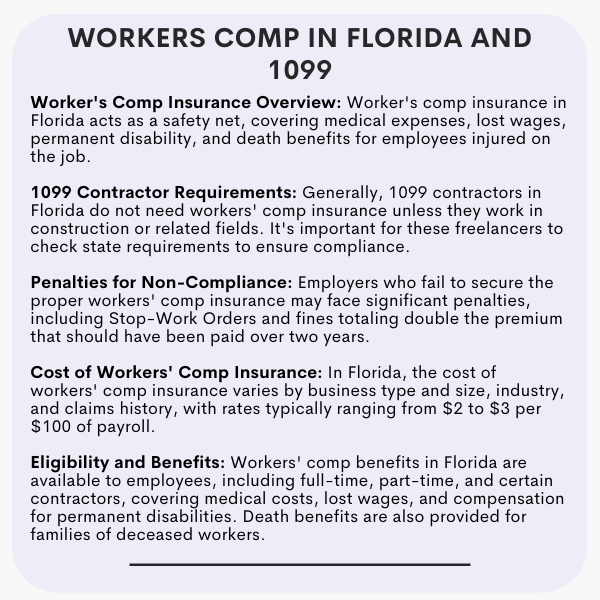

Workers’ comp insurance in Florida is like a safety net for employees who get injured on the job or fall ill due to work duties. It’s like having a superhero protection shield that covers medical expenses, lost wages, permanent disability, and even death benefits in case the worst happens. Imagine, no more worrying about paying hospital bills or surviving without a paycheck.

Workers’ comp has got you covered!

Recent development as of 8/10/2025: Florida has not enacted major changes to its workers’ compensation laws regarding 1099 independent contractors in the past couple of years, and most independent contractors are still not required to carry workers’ comp coverage unless they work in construction or similarly high-risk fields. In the construction industry, Florida law effectively forbids treating workers as 1099 contractors unless they are bona fide business owners with a valid exemption, contractors must ensure all on-site workers are either covered as employees or have filed for an exemption.

A 2023 regulatory update now requires insurers to verify that a subcontractor has non-exempt employees before charging additional premium to a general contractor’s policy. Florida authorities have also stepped up compliance: in the 2023–24 fiscal year, enforcement efforts led to over 8,400 previously uninsured workers (often misclassified as contractors) being brought under workers’ comp coverage. Meanwhile, gig-economy workers remain classified as “marketplace contractors” under a 2018 law and are treated as independent contractors (not employees) for workers’ comp purposes, notably, no new legislation in 2024 or 2025 has altered these fundamental rules for 1099 contractors, so the existing coverage requirements and exemptions continue to apply.

Are you an independent contractor in Florida trying to determine if you need workers compensation insurance?

You’re not alone – this is a common question that many freelancers and business owners have.

While there are some misunderstandings about the requirements of workers comp laws in Florida, the answer is actually simpler than you think.

So start up your coffee pot and get comfortable with us as we unpack everything you need to know about whether or not it’s necessary for 1099 employees in Florida to carry workers’ comp insurance!

The million-dollar question for Florida business owners and their employees is: do I need workers compensation insurance as a 1099 contractor?

The good news is that the Floridians don’t need to be all flummoxed about it because, in most cases, the answer is no.

To ensure that you are complying with all relevant Florida laws, however, be sure to double-check your situation against the state requirements and put any concerns out of your mind.

If you’re a 1099 contractor in Florida, your paperwork might be light until it comes time to work construction. If that’s the case – don’t leave home without worker’s compensation!

Many independent contractors in Florida evade the tedious paperwork of getting a worker’s compensation program. But if these freelancers work under construction or any related field, they are not given an option and must acquire such policies to stay compliant with state regulations.

Knowing whether or not you require workers’ comp coverage can be a tricky business– sort of like deciding whether or not you should order dessert after dinner!

What Are The Penalties For Not Having Workers Comp Insurance in Florida?

Employers must ensure they have the correct protection in place or risk facing a stern penalty. Civil enforcement action, such as Stop-Work Orders suspending operations and requiring payment of fines can be imposed for not complying with the law. This is one situation where it pays to make sure you are onside!

Employers who fail to comply with their reporting obligations face hefty fines – double the amount they should have paid in premium over a two-year period.

Employers may receive a Stop-Work Order if they try to dodge their obligation of proper payment for Workers’ Compensation Insurance by fudging payroll, disguising employee duties or similar tactics.

How Much Will Workers Comp Insurance Cost Me in Florida?

The cost of Workers’ Compensation Insurance in Florida depends on a number of factors, including the type and size of business, the industry in which it operates and the claims history. Generally speaking, businesses can expect to pay $2 – $3 for every hundred dollars of payroll. Employers should also be aware that failure to adhere to legal regulations.

Who is Eligible for Workers Compensation Benefits in Florida?

Workers’ Compensation Insurance in Florida provides benefits to any employee who suffers a work-related injury or illness. This includes both full-time and part-time employees, as well as independent contractors and subcontractors.

Injured workers may be eligible for medical costs, lost wages and compensation for permanent disabilities resulting from their injuries. Additionally, employers are required to provide death benefits for families of workers who succumb to their injuries in Florida.

In order to receive these benefits, an employee must first file a claim with the Florida Division of Workers’ Compensation.

Claimants must then prove that their injury or illness was caused by a work-related activity and that they are unable to return to their job. If a claim is approved, the employee will receive benefits until their medical condition improves or they reach maximum medical improvement (MMI).

The amount of compensation awarded to injured workers depends on the severity of their injury and may include payment for past and future medical bills, lost wages and job retraining costs. Additionally, employers may be required to pay death benefits to the families of workers who succumb to their injuries in Florida.

It is important for employees to be aware of their legal rights and responsibilities when filing a workers’ compensation claim in Florida.

Employees who have questions or concerns about the process should seek legal advice from an experienced workers’ compensation attorney in Florida. With an experienced lawyer on their side, employees can rest assured that their rights will be defended and that they will receive the compensation they deserve for any workplace injury or illness.

If an employee does not have legal representation, it is important to remember certain tips when filing a workers’ compensation claim in Florida.

They should always keep detailed records of their medical treatment, including doctor visits, medications prescribed, and any other treatments received. Employees should also keep records of any lost wages due to their injury or illness, as well as any out-of-pocket expenses incurred as a result of their condition.

Finally, it is important to understand the deadlines for filing a claim and appeal so that they can ensure their rights are fully protected.

How Do I File a Workers Compensation Claim in Florida?

A worker should contact their local district office of the Division of Workers’ Compensation to file a claim.

They will need to provide information such as medical records, income statements, and detailed descriptions of how their condition was caused by work-related activities. Once all information has been provided, the district office will review and determine whether or not the claim is valid. If it is, the worker will be notified and receive benefits according to their individual situation.

If a claim is denied, an appeal can be filed within 30 days of the denial. The appeal must include additional evidence, supporting information, and arguments for why the decision should be overturned in order to have a chance of success. It is possible to appeal a denial up to three times.

Once an appeal is approved, the worker can receive benefits as outlined in their individual case. It’s important for workers to understand their rights and what options are available to them when filing a workers’ compensation claim.

From building new homes, to keeping infrastructure up-to-date and safe – construction workers play an essential role in making our country the forefront of progress.

Without them, we wouldn’t have cities bustling with life or industry that moves us forward each day!

In 2021, the U.S. Bureau of Labor Statistics gave us a startling statistic: over two and a half million workers in private industry suffered from accidents or illnesses – testifying to precisely how challenging life on the job can be!

Construction crews brave the risks of a hazardous occupation every day—from operating heavy machinery to erecting towering edifices. Despite safety regulations and precautions, too many workers are still being injured or killed in construction-related accidents annually.

It’s an unfortunate reminder that no amount of preparation can fully protect those hardworking men and women risking their lives on job sites each day.

Construction sites can be dangerous environments, both due to the nature of work and a wide variety of accidents that may occur. But despite project variations, there is an underlying trend amongst construction site related injuries – one which when understood could help boost safety protocols even further.

From minor scrapes to grave fatalities, construction sites are no strangers to dangerous hazards. Here we look at some of the most notorious accidents and injuries associated with this occupation.

Construction workers who have suffered from an on-the-job injury could be experiencing tremendous physical, financial and emotional strain. If you are in this position, Florida legislation has ensured your rights to justice and protection so that you can continue forward with the best outcome possible.

It’s essential to know what those protections entail – don’t hesitate to become informed of every right available!

Construction sites can be dangerous places—but what types of injuries are especially prone to occur? Slips, trips, and falls top the list due to slippery surfaces or debris littered on walkways. In addition, strains from manual labor as well as cuts and lacerations may also present a threat while working with heavy machinery.

Be sure that safety measures are taken when tackling any construction project!

Construction workers face serious potential dangers on the job, from slips and falls to hazardous materials.

According to OSHA, these are the most common sources of injury: electric shock; falling objects; scaffolding collapse or other structure failures; exposure to harmful chemicals or airborne particles; overexertion or fatigue-related incidents due to inadequate safety practices such as not wearing personal protective equipment (PPE); vehicle collisions with construction sites/workers walking in work zones without proper warning signage.

It’s imperative for employers and those working at a site adhere strictly to best practice guidelines that ensure safe conditions for everyone involved.

1. Construction Site Electrocution Injuries

Construction work is often unavoidably close to high-voltage electricity sources, leaving workers dangerously exposed.

Despite protective protocols and warnings aimed at prevention of injury, electrocution accidents still occur on job sites – underscoring the need for extra caution when near power lines or other energy generating equipment.

Electrocution can be a devastating experience, with possible consequences ranging from burns to cardiac arrest and nerve damage.

How Do Construction Workers Get Electrocuted?

In everyday life, contact with metal objects is unavoidable. But when those same items become electrically charged from power sources like ladders and wires, they can put others in danger of electrocution or shock.

That’s why it pays to be extra careful around energized trucks and other vehicles, as well as tools that may inadvertently cut through electricity-charged metals pipes or wires!

Working on a construction site can be incredibly dangerous for workers, as evidenced by the number of workers who are injured or even killed each year due to electrocution. Among workers compensation Florida claims in high-risk jobs, those related to electrocutions hover near the top of the list.

If you or someone you know has been injured at work from an electrical shock, it’s important to understand your rights and seek appropriate compensation.

Suffering an electric shock at work can be a traumatic experience, especially in more serious cases. Even if you don’t have any electrical expertise or certifications, it’s possible to make a claim for damages should the incident occur as due to negligence such as faulty equipment maintenance and lack of adequate training.

With enough awareness and prevention measures, we can help reduce the number of workers suffering from preventable electrocution injuries at construction sites.

To help prevent such tragedies, OSHA regulations are in place that focus on everything from addressing safety requirements to the proper design of electrical equipment. Additionally, utilizing protective devices like insulation is essential for maximum protection against electrocutions.

2. Fall Injuries on Construction Sites

Working on construction sites comes with a raft of potential dangers, one being falls from great heights. Construction sites can be hazardous, as falls are a common cause of injury. Falls account for around 35% of all accidents at these job sites and can result in serious injury or death if not prevented correctly.

To help prevent these accidents, workers must pay extra attention to uneven surfaces; practice proper mounting and dismounting from machinery; make sure ladder use is safe; and always utilize fall protection equipment for added security.

Factors that impact the severity are how far to the ground a worker was when they fell, as well as whether any safety equipment is present, such as protective scaffolding or ladders.

Unfortunately, many times no security measures exist because workers often build up projects entirely from scratch making it hard to strategically plan ahead against risks like falling off roofs, chimneys etc…

Even with safety measures in place, workers still need to be aware of the potential risks and take any necessary precautions to prevent an accident from occurring. It is essential for employers to provide training and instruction on how to properly use protective equipment and recognize red flags that may lead to a hazardous situation. Employers must continue to update the protocols in order.

In 2020, a grim statistic emerged: one out of every five workplace deaths occurred in the construction industry. More specifically, falls to lower levels accounted for an alarming 46.1% of all fatal slips and trips that year. Making matters worse – this number remains consistent with past years’ trends according to U.S Bureau of Labor Statistics data!

Broken Bones From Construction Site Falls

Falls can cause more than just a bruise or scrape – they may lead to broken bones, which vary in severity from minor fractures to major breaks.

Painful and frightening at times, treatment of broken bone injuries range from simple bandaging to complex surgery, depending on the location and extent of damage sustained by the individual.

Back Injuries In Construction

One of the most common types of injuries caused by falls on construction sites is back injuries. Back injuries can range from minor strains and sprains to more serious injuries such as herniated discs or spinal cord damage.

Falls from heights are a particularly common cause of back injuries in construction workers.

Back injuries are the costliest construction-related hazard, with 25% of all reported cases annually. Unfortunately, even one injury can be devastating; leading to an average seven workdays away from their job, as well as increased risk for permanent damage and career ending complications.

Spinal Cord Injuries Caused by Falls on Construction Sites

Spinal cord injuries caused by falls on construction sites amount to more than their fair share of workers compensation claims in Florida alone.

Spinal cord injuries, especially those that cause paralysis, have a serious impact on the quality of life of those affected.

An injured construction worker might not only feel significant physical pain and suffering, but also worry about what measures their employer has put in place for workers compensation. That’s why it’s important for workers to know and understand their rights, especially if they have been injured at work.

3. Machinery Injuries on Construction Sites

Working on construction sites comes with a raft of potential dangers, one being falls from great heights. Construction sites can be hazardous, as falls are a common cause of injury. Falls account for around 35% of all accidents at these job sites and can result in serious injury or death if not prevented correctly.

Despite the remarkable advances made in terms of efficiency, working with heavy machinery still comes packed with its own set of hazards.

Accidents involving these machines are unfortunately one of the leading causes for workplace mishaps on construction sites – a reminder that safety should always be top priority!

Construction machinery accidents can happen when you least expect it: health risks, malfunctioning equipment, and unsafe conditions all pose potential dangers. Being aware of the common hazards will help protect workers on-site from any unwelcome surprises.

What Are Common Construction Machinery Related Injuries?

Despite the remarkable advances made in terms of efficiency, working with heavy machinery still comes packed with its own set of hazards.

Accidents involving these machines are unfortunately one of the leading causes for workplace mishaps on construction sites – a reminder that safety should always be top priority!

Construction machinery accidents can happen when you least expect it: health risks, malfunctioning equipment, and unsafe conditions all pose potential dangers. Being aware of the common hazards will help protect workers on-site from any unwelcome surprises.

4. Construction Site Collapse Injuries

Construction sites can be hazardous for workers due to the potential of building and ground collapses.

This tragedy, which is often devastating in both human cost and financial expense, could occur when structures are poorly maintained or undermined by geological instability such as shifting soils.

Before a skyscraper can reach for the sky, construction workers must start below ground. With dangers of cave-ins and collapses looming overhead, these brave contractors take on an incredibly risky job to dig foundations, run utilities and lay down groundwork.

The potentially devastating consequences of a building or ground collapse are not to be taken lightly; many have found that even the most skilled construction worker is no match for Mother Nature.

Trench Collapses in Construction

From suffocation due to mud and soil caving in, to head trauma resulting from accidental falls – these disasters can typically result in deathly outcomes if precautionary safety measures aren’t enforced.

To ensure workplace safety of those working in excavations, and compliance with OSHA regulations, employers are required to provide shoring, shielding or sloping protection when necessary. This will provide a critical defense against cave-ins.

Sadly though, far too many supervisors ignore installing such safeguards due to time and cost pressures – leaving workers without this vital safeguard against soil walls.

Foundation Collapses in Construction

When foundations lack proper design and construction, the weight of a building can cause catastrophic collapse. Without stable support beneath it, any structure is at risk for instability– putting workers in danger from floor to ceiling.

Rooftop cave-ins can be devastating, yet they are often the result of poor planning decisions and shortcuts.

A combination of heavy machines or loads on a structure without sufficient supports, cost-saving measures such as low quality building materials, and overlooked risk factors during inspections could all lead to catastrophic consequences.

5. Construction Site Trip Injuries

Construction sites can be dangerous places if you don't take the right precautions – particularly when it comes to slips, trips and falls.

Wet surfaces, debris-laden floors, loose ladders or scaffolding structures are just some of the common hazards that could lead to serious injury on a construction site – not forgetting more unexpected dangers such as vehicle-related risks and weather conditions.

And all this is before discussing potential obstacles created by hoses left lying around unsecured in dimly lit areas! It’s always important to stay vigilant while carrying out any kind of work at a building site.

A trip can happen in the blink of an eye, but the consequences may last much longer. Tripping is a common cause of injuries ranging from mild to severe – traumatic brain injuries (TBIs), spinal cord damages, broken hips or pelvis fractures, shoulder and neck injury trauma, limb breaks and even torn ligaments are all risks when you stumble.

What Does OSHA Consider a Tripping Hazard?

Working environments can contain hidden dangers – any object in the path of a person’s feet that could trip them or cause traction loss is considered a tripping hazard. Common examples include cables, paper, boxes, and hoses left carelessly lying around pathways.

OSHA urges employers and employees to keep work environments safe by making sure hazardous holes or openings are properly covered.

Openings 30 inches tall and 18 wide need covers, railings for tripping prevention, as well as toe boards if there’s the possibility of tools falling into it or people passing under.

All these measures ensure any workplace remains secure from falls and accidents!

6. Construction Site Vehicle Accidents

Construction work is often seen as a rewarding career despite the risk of injury.

Aside from falls and machinery, many construction personnel are unaware that site vehicles can be equally if not more dangerous to workers on-site. Knowing the risks associated with every aspect of your job will help ensure you stay safe while at work!

Construction site vehicles can cause life-altering injuries, putting you out of commission for an indefinite period that could span weeks to months or even beyond.

Construction sites are home to an array of heavy vehicles and earth-moving equipment, which help make large projects easier for workers.

Yet these powerful machines can also be a potential hazard in inexperienced hands or when passing through hazardous zones – the safety of those onsite must always take priority.

With over 3,000 lives lost and 40,000 people injured each year from vehicle incidents at work zones – it’s clear that this is a serious risk to employees.

OSHA emphasizes the importance of proper safety training when vehicles are present in order to protect workers on-site.

Construction Site Vehicle Collision Accidents

Construction workers face an unnecessary risk of harm due to reckless driving and accidents.

Collisions or rollovers are the most common types of vehicle mishaps, but they can be particularly hazardous for construction personnel who don’t have any protection from a cab inside their rigs.

Plus, these heavy-duty vehicles tend to cause extensive damage when involved in crashes with other automobiles or pedestrians onsite.

Construction Site Vehicle Pinning Injuries

From construction sites to warehouses, workers can all too easily become the victims of a dangerous situation: pinning.

Without vigilant attention from operators or brakes that fail to engage in time, vehicles and heavy machinery might roll into those on foot nearby – leading to awful crush injuries as they’re pinned between objects.

Construction Site Vehicle Back-Up Accidents

Every year, 70 workers tragically lose their lives due to back-over incidents that were preventable.

These accidents happen when a vehicle strikes someone walking or standing behind it and are often caused by drivers who fail to properly check the area around them for hazards such as people in blindspots not visible from the driver’s seat.

Knowing these risks is key so steps can be taken towards keeping everyone safe on job sites everywhere!

7. Construction Site Repetitive Motion Injuries

What Are Repetitive Motion Disorders?

Repetitive motion disorders (RMDs) can be the result of normal work and daily activities, but they occur when too many repetitions are done without interruption.

Repetitive strain injuries are a growing concern in many workplaces, especially those that involve frequent repetitive motions.

Even the activities we do for leisure can cause damage if performed too often without proper protection or conditioning – so it’s important to be aware of potential risks and take steps to remain safe while performing any type of work duty!

Industries where employees are exposed to the dangers of repetitive tasks have an increased risk for injury.

These jobs often involve continuous, repeated motions that can create physical strain over time. To ensure safety and well-being in these industries, it is essential workers remain aware of potential hazards associated with their job duties.

Transportation related jobs, food preparation workers, manufacturing positions, retail positions, entertainment workers, office workers, sewing positions, construction workers, and more – are all jobs that require repetitive motion.

Posture, motions such as twisting an arm or wrist, overexertion and muscle fatigue all contribute to RMDs like carpal tunnel syndrome; tendonitis in elbows, shoulders, or wrists; radial/ulnar epicondylitis (tennis elbow); trigger finger/thumb; rotator cuff injury and De Quervain’s Syndrome.

Working without taking the time to recover can put workers at a higher risk of serious construction hazards – musculoskeletal disorders (MSDs) being one of them.

These injuries, such as shoulder and low back strain, carpal tunnel syndrome or tendonitis usually begin with minor aches and pains but if ignored they could worsen over time leading to long-term damage.

Being aware of what causes these symptoms is key for avoiding unnecessary complications in the future!

Protecting your employees is not only the responsible thing to do – it can save you from potentially devastating financial costs, too.

Without a workers’ compensation program in place, small businesses are particularly vulnerable when faced with paying out-of-pocket for an employee’s strain injury or legal fees associated to such matters.

Ensure that both yourself and your staff have all bases covered: consider investing in our workers’ comp program today!

Workers compensation is a state-mandated insurance program that provides benefits to employees who are injured or become ill as a result of their job.

If you’re an employer, it’s important to have workers comp coverage in place to protect your business and employees.

At OCMI, we’re experts in PEO brokerage and can help you find the best and most affordable PEO program for your business. So if you’re looking for the best workers comp coverage at the best price, look no further than OCMI!

We’ll make sure you get the protection you need at a price that fits your budget.

And remember: to prevent injury or death from occurring onsite, it’s critical that rigorous safety protocols are followed during construction projects of all sizes.

Who Pays For Workers Comp Medical Bills? Injuries happen, and when they happen on the job, it can be stressful to figure out who is responsible for workers comp medical bills.

The answer isn’t always straightforward, but thankfully there are some easy ways to figure out who’s footing the bill. Let’s dive in and get to the bottom of this!

What If I Get Injured at Work?

If you get hurt at your workplace, don’t brush off a workplace injury, even if it’s minor!

Neglecting your medical needs can cost you greatly down the road. Acknowledge and document any injuries immediately to ensure both your health – and legal rights – are in good hands.

If an employer is reluctant, you have the right to select a doctor of choice for diagnosis without expense on your part – what could be better?

Get ahead of potential unpleasantries before they become serious so that everything stays safe, healthy & legally sound!

Don’t wait for your work-related injury or condition to get even worse – take action now and document the evidence! Protecting yourself is always a priority, so don’t delay in seeking an evaluation.

What if I Can't Work After My Injury?

Sometimes injuries can prevent an employee from returning to work for an extended period of time or even permanently. In these cases, employers may provide additional financial assistance beyond just covering medical costs.

Depending on your state’s laws, you may qualify for wage replacement benefits—also known as temporary disability or lost wage benefits—which will provide you with a portion of your normal salary while you recover from your injury or illness and are unable to work.

In addition, some states also offer permanent disability benefits which provide long-term financial assistance if you are unable to return to work due to your injury or illness.

Your employer should be able to provide more information about which benefits are available in your particular state so that you can make sure you are taking full advantage of them if needed.

Can My Employer Pay For My Medical Bills Even Though I Have Workers Comp?

The following applies to situations where workers comp insurance is part of the scenario.

Should you file a workers’ compensation claim even if your employer offers to pay your medical bills?

The answer is “definitely YES!” The rise of workplace injuries has sparked a concerning trend: employers attempting to talk employees out of filing for their entitled workers’ compensation insurance.

Employers are always on the lookout for innovative ways to minimize their losses and control costs, so it’s no surprise many have turned to wondering if paying medical bills directly can help save money. But before attempting such a creative strategy with workers’ compensation expenses, employers should consult the Department of Labor and Industry.

But don’t be fooled – you deserve the coverage, no matter what any employer may say!

When it comes to medical bills for injured employees, even the tiniest expenses should be covered by insurance – not employers! The employers should pay the insurance coverage and not the medical bills.

When Should My Employer Report My Work Injury?

According to Section 440.185, Florida Statutes, Your employer needs to report your workplace injury as soon as they know about it – and no later than 7 days after.

The insurance company then has three days to send you an informational brochure outlining what’s going on from every angle, including all the details of workers’ comp laws that apply in this case. Knowing everything is key for getting back on track faster!

If your employer isn’t doing their part to report an injury, you don’t have to take it lying down. Let the insurance company know what happened by taking matters into your own hands – but if that’s too much of a hassle, get in touch with EAO and let them lend a helping hand at (800) 342-1741 or email them at: wceao@myfloridacfo.com

Private health insurance may seem like a lifesaver, but if you’ve been injured on the job it could be hazardous to your wallet. Claims for work-related injuries won’t just stop payment – they’ll hit reverse! The insurer will demand that any amount previously taken care of is paid back. In those cases, filing workers’ compensation might end up saving you from an awkward financial situation and hefty co-payments down the line.

Figuring out who pays for workers comp medical bills doesn’t have to be complicated! Generally speaking it’s usually the employer’s responsibility (or their insurance provider) but this can vary from state-to-state so it’s important to check with your local laws regarding worker’s compensation before making any assumptions about who should pay for your treatment costs after an accident at work.

Knowing what options are available can help ensure that you receive all necessary care without having to worry about large out-of-pocket expenses down the line! So keep those purses tight and your workforce healthy.

Why You Need to Have Workers Comp Insurance

Here are five reasons why having workers compensation insurance is essential for any business owner. Ah, the joys of entrepreneurship. You get to make all the decisions and watch your business grow. But with all the freedom comes a certain amount of responsibility—namely, making sure you have workers comp insurance for your employees.

While it’s true that having workers comp can be expensive, it’s also essential if you want to keep your business running smoothly.

Sure, owning your own business can seem glamorous – but it definitely comes with high stakes! Not only do you have to worry about working injury insurance and payroll taxes that were never even in the back of your mind before, but staying competitive in today’s market is a daunting task.

There are sure rewards for successfully being your own boss and taking charge of your career, though, so don’t get too intimidated by the high risks associated with such an endeavor.

If you truly believe you’re cut out for entrepreneurship and you’re willing to put in the hard work it takes to protect yourself from pitfalls and roadblocks, go for it! You could end up loving every moment of business ownership – high risk or no high risk.

Running a business can be a minefield and protecting it should be one of your top priorities. You can start by being proactive, setting up protocols and backup plans along with sensible regulations and having an overall security strategy in place.

Workers Compensation protects your business from unforeseen expenses: Let’s face it—you never know when an accident might occur at work and result in costly medical bills or lost wages for employees.

With workers comp insurance, those expenses are covered so you don’t have to worry about footing the bill yourself.

So take a little time to understand your risks and devise plans to counter them—your future self will thank you for it!

2. Workers Comp Keeps Employees Safe

Let’s face it—accidents happen, no matter how careful we try to be. You know the saying, safety first! One of the best ways to keep employees safe while they are at work is through workers compensation insurance.

Workers comp ensures that if an employee is injured on the job, they will be taken care of and not stuck with a massive medical bill that could potentially bankrupt them.

Workers comp helps protect employers and employees alike by providing reimbursement for lost wages, medical expenses and other types of benefits in the event that an employee is injured on the job.

With this program in place, businesses have peace of mind that their employees are taken care of should any workplace accidents occur.

It’s a win-win situation – because who doesn’t want their staff to be able to perform their day-to-day duties without worry? Workers comp is like a guardian angel watching over them from above.

3. Workers Comp Shows That You Care For Your Employees

No matter what business you’re in, the best employers have three things in common – they understand that their staff are their most important resource, they create a positive work environment and they are always willing to go the extra mile for both their employees and customers.

Those employers who value their staff will end up with a more engaged workforce who care about the success of the company.

It’s no surprise that those companies usually outperform their competitors and reap the rewards! When it comes down to it, happiness in the workplace is just as important as any other business metric – and happy employees are probably the best employers out there.

So that is why having workers comp shows your employees that you care. Offering workers compensation shows your employees that you value their safety and well-being and are willing to invest in keeping them safe while they work for you.

This can help create a sense of loyalty among your staff and foster a positive working environment overall.

4. Workers Compensation Can Avoid Litigation

It Could Help Avoid Litigation. If an employee is injured on the job without workers compensation insurance, they may be inclined to take legal action against your business in order to recoup their losses or seek damages for their injury—something which could be avoided by having workers comp insurance in place beforehand.

Keeping your business safe and sound from allegations may not be the most exciting of tasks, but it’s certainly one of the most important.

Investing in measures that protect your company from claims and defending yourself with good legal services will help you rest easy knowing you are prepared for any situation that comes your way.

Don’t get stuck carrying the weight of damaging accusations – take proactive measures to shield yourself and keep your business running without a hitch.

If one of your employees gets hurt on the job and decides to sue you for negligence or failure to provide adequate safety protocols.

This could lead to major financial losses for your business if you’re found liable in court—unless you have workers comp insurance, which could help protect you from these kinds of claims (depending on where you live).

5. Workers Comp Is Required in Most States

It’s no wonder that most states require Workers Comp – after all, blunders can happen at the office, and it’s comforting to have some sort of plan in place for protecting employees (not so much for any destroyed printer cartridges or spilled coffee).

It’s a little like playing chess: months of work can be lost in one misstep without protection.

So next time you’re feeling lucky and decide to go without Workers Comp, just remember what that old saying goes: “you don’t miss your Workers Comp until it’s gone!”

Conclusion:

At the end of the day, having proper workers compensation insurance is essential for any business owner who wants to protect both themselves and their employees from unforeseen accidents or injuries on the job.

Not only does it offer peace of mind but it also helps ensure that everyone stays safe while working hard towards achieving success together as a team! So don’t wait another minute; make sure you get adequate coverage today!

What is Workers' Compensation Insurance and Who Is It For?

Who Is Exempt From Workers’ Compensation Insurance in Florida?