Nonprofits: Why Workers’ Comp Insurance is Essential

Non-profit organizations are essential to society, as they work tirelessly to promote a wide range of causes that benefit the community. However, like any other business, non-profits must ensure that their employees are protected from workplace injuries and illnesses.

Workers’ compensation insurance is a crucial component of any comprehensive employee protection plan, but many non-profits may not be aware of the legal requirements or benefits of this type of insurance.

In this blog post, we will explore the topic of workers’ compensation insurance for non-profit organizations, including who needs it, the benefits of having it, and how to obtain it. Whether you are an established non-profit or just getting started, this post will provide you with valuable insights to help protect your employees and your organization.

Explanation of Workers' Compensation Insurance

Workers’ compensation insurance is like the superhero sidekick of the business world. It’s a safety net that helps protect employees and employers in the event of a workplace injury or illness.

This type of insurance provides financial and medical benefits to employees who are injured on the job, while also protecting employers from costly lawsuits. Think of it like a band-aid for a boo-boo or a hug from your mom after falling off your bike.

It’s there to make everything better when things go wrong. In this blog post, we’ll take a closer look at workers’ compensation insurance and how it can benefit non-profit organizations.

Workers’ compensation insurance is like the superhero sidekick of the business world. It’s a safety net that helps protect employees and employers in the event of a workplace injury or illness.

This type of insurance provides financial and medical benefits to employees who are injured on the job, while also protecting employers from costly lawsuits. Think of it like a band-aid for a boo-boo or a hug from your mom after falling off your bike.

It’s there to make everything better when things go wrong. In this blog post, we’ll take a closer look at workers’ compensation insurance and how it can benefit non-profit organizations.

Alrighty, let’s get down to business! In this blog post, we’re talking about workers’ compensation insurance for non-profit organizations. Here’s what you need to know:

~ Workers’ compensation insurance is a safety net that helps protect employees and employers in the event of a workplace injury or illness.

~ If you have employees, then you most likely need workers’ compensation insurance.

~ Workers’ compensation insurance provides financial and medical benefits to employees who are injured on the job, while also protecting employers from costly lawsuits.

Now, let’s dive a little deeper into the world of workers’ compensation insurance and explore what it is, who needs it, and how it works.

Understanding Workers' Compensation Insurance

Workers’ compensation insurance is like a magical unicorn that protects employees and employers from the perils of workplace injuries and illnesses.

In its simplest form, workers’ compensation insurance is a type of insurance that provides benefits to employees who are injured on the job. But, it’s also so much more than that. It helps protect employers from lawsuits, provides medical care to injured employees, and helps ensure that employees are able to return to work as soon as possible.

It’s like having a superhero on your side, fighting for justice and fairness in the workplace.

Who Needs Workers' Compensation Insurance?

Well, as we mentioned earlier, if you have employees, then you most likely need workers’ compensation insurance.

This includes non-profit organizations of all shapes and sizes. It doesn’t matter if you have one employee or one hundred employees – if they’re on your payroll, then you need to protect them.

Workers’ compensation insurance is a legal requirement in most states, so it’s important to make sure that your non-profit is in compliance with the law. And, even if it’s not required by law in your state, it’s still a smart business decision to have it.

Do You Need Workers Comp For Volunteers?

The answer to this question really depends on the individual state laws.

Most states do not require non-profits to provide workers’ compensation insurance for volunteers. However, it’s always a good idea to check with your local Department of Labor or Insurance Commissioner before making any decisions about workers comp coverage for volunteers.

It’s also important to keep in mind that volunteers may still be eligible for workers’ compensation benefits in some cases. For example, if a volunteer is injured on the job or becomes ill due to their work at your non-profit, they may be able to receive workers’ comp benefits from your state’s fund.

The Benefits of Workers' Compensation Insurance

Ah, the juicy stuff – the benefits of workers’ compensation insurance. So, what’s in it for you and your non-profit? Well, there are quite a few benefits, including:

Workers' compensation insurance provides financial benefits to employees who are injured on the job. This includes coverage for medical expenses, lost wages, and rehabilitation costs. By having this insurance in place, your non-profit won't be held responsible for covering these costs out of pocket.

If an employee is injured on the job and decides to sue your non-profit, workers' compensation insurance can help protect you from costly legal fees and damages. It provides coverage for legal defense costs and can help settle claims out of court.

Workers' compensation insurance helps protect your employees by ensuring that they receive the medical care they need to recover from their injuries. This includes coverage for doctor visits, hospital stays, surgeries, and more. It also helps ensure that injured employees are able to return to work as soon as possible, reducing the impact of their injury on their life and livelihood.

Finally, having workers' compensation insurance in place gives you and your non-profit peace of mind. You'll know that your employees are protected, that you're in compliance with the law, and that you have a safety net in place in case something goes wrong. And, let's face it, when you're running a non-profit, peace of mind is priceless.

So, there you have it – the benefits of workers’ compensation insurance for non-profit organizations. It’s an important investment in the safety and well-being of your employees and your organization.

Non-Profit Organizations and Workers' Compensation Insurance

Now, let’s talk specifically about non-profit organizations and workers’ compensation insurance. Here are some things you need to know:

Are Non-Profit Organizations Required to Have Workers' Compensation Insurance?

The answer to this question depends on the state you’re in and the number of employees and volunteers you have. In most states, non-profit organizations are required to have workers’ compensation insurance if they have one or more employees. However, there are some exceptions to this rule, so it’s important to check the laws in your state to make sure you’re in compliance.

What Types of Non-Profit Organizations Need Workers' Compensation Insurance?

All types of non-profit organizations need workers’ compensation insurance if they have employees. This includes charities, foundations, religious organizations, and more.

It doesn’t matter if you’re a small non-profit with just a few employees or a large organization with hundreds of employees – if they’re on your payroll, then you need workers’ compensation insurance.

Common Misconceptions About Workers' Compensation Insurance for Non-Profits

There are a lot of misconceptions out there about workers’ compensation insurance for non-profit organizations. One of the biggest misconceptions is that non-profits are exempt from workers’ compensation insurance requirements because they’re not in it for profit.

This is simply not true. Another misconception is that workers’ compensation insurance is too expensive for non-profits. While it’s true that insurance costs can be a concern for non-profits, there are many affordable options available.

The Risks of Not Having Workers' Compensation Insurance for Non-Profits

Finally, let’s talk about the risks of not having workers’ compensation insurance for non-profit organizations. If you don’t have this insurance in place and one of your employees is injured on the job, you could be facing serious financial and legal consequences.

You could be held responsible for covering the costs of their medical care and lost wages, which could be a huge financial burden for your non-profit. Additionally, if the injured employee decides to sue your non-profit, you could be facing costly legal fees and damages. It’s simply not worth the risk to go without workers’ compensation insurance.

Benefits of Workers Comp Insurance for Non-Profit Organizations

So, you want to know about the benefits of Workers’ Compensation Insurance for Non-Profit Organizations?

Well, one major benefit is that it protects employees from workplace injuries and illnesses. By having this insurance in place, employees can have peace of mind knowing that they will be taken care of if they are injured on the job. Plus, it can help cover medical expenses and lost wages.

Another benefit of Workers’ Compensation Insurance for Non-Profits is that it ensures compliance with legal requirements. In many states, it is mandatory for employers to carry this type of insurance. By having it, non-profits can avoid legal trouble and hefty fines that come with non-compliance.

Did you know that Workers’ Compensation Insurance can protect non-profits from expensive lawsuits? That’s right! If an employee is injured on the job and the non-profit doesn’t have Workers’ Compensation Insurance, the employee could potentially sue for damages. This can be costly and time-consuming for the non-profit. But with insurance in place, the non-profit is protected and won’t have to worry about expensive legal fees.

Lastly, Workers’ Compensation Insurance supports the mission of non-profit organizations. By providing a safe and secure work environment for employees, non-profits can focus on what they do best: making a difference in the community. It also shows that the non-profit values their employees and is committed to their well-being, which can help attract and retain talented staff.

How to Obtain Workers' Compensation Insurance for Non-Profit Organizations

One way is to work with insurance brokers who specialize in non-profits. These experts can help non-profits navigate the complex world of insurance and find the best policy for their needs.

Another important step in obtaining Workers’ Compensation Insurance is to compare policies and rates. Non-profits should shop around and compare different options to find the best coverage at the most affordable price. Don’t forget to read the fine print and understand any exclusions or limitations.

Understanding the coverage options is also key. Non-profits should make sure they know exactly what their policy covers and what it doesn’t. For example, some policies may not cover certain types of injuries or illnesses. It’s important to be aware of these details so that non-profits can make informed decisions.

Lastly, non-profits should know how to file a workers’ compensation claim. In the unfortunate event that an employee is injured on the job, non-profits should have a clear process in place for filing a claim. This can help ensure that the employee gets the care they need and that the non-profit is protected from potential legal action.

Let’s recap the key points: Workers’ Compensation Insurance protects employees from workplace injuries and illnesses, ensures compliance with legal requirements, protects non-profits from expensive lawsuits, and supports the mission of non-profit organizations. To obtain this insurance, non-profits should work with insurance brokers who specialize in non-profits, compare policies and rates, understand coverage options, and know how to file a workers’ compensation claim.

My final thoughts on Workers’ Compensation Insurance for Non-Profit Organizations? It’s an important investment for any non-profit. By providing a safe and secure work environment for employees, non-profits can focus on their mission and make a positive impact in the community. Plus, it shows that the non-profit values their employees and is committed to their well-being.

So, my call to action for non-profit organizations is simple: obtain Workers’ Compensation Insurance. Don’t wait until it’s too late. This insurance is crucial for protecting your employees, your organization, and your mission.

Contact us at OCMI to speak with an insurance broker who specializes in non-profits today and start the process of obtaining Workers’ Compensation Insurance. Your employees will thank you!

Common Workers’ Comp Claims and How to Avoid Them

Workplace injuries can be a costly and difficult experience for both employees and employers. Fortunately, many common workers’ comp claims can be prevented with some basic precautions and preventative measures.

In this blog post, we’ll explore the most frequent types of workers’ comp claims and provide tips on how employers can reduce the risk of workplace injuries. By prioritizing workplace safety and taking steps to prevent injuries, both employees and employers can benefit from a safer, healthier work environment.

So let’s dive in and learn how to avoid some of the most common workers’ comp claims!

Explanation of What Workers' Comp is And Why it's Important

Workers’ compensation (commonly known as workers’ comp) is a type of insurance that provides benefits to employees who suffer job-related injuries or illnesses. It is a no-fault system, which means that injured employees are generally entitled to benefits regardless of who was at fault for the injury.

Workers’ comp benefits can cover medical expenses, lost wages, rehabilitation costs, and other related expenses.

The purpose of workers’ comp is to protect both employees and employers. For employees, it provides financial support and access to medical care if they are injured on the job. For employers, workers’ comp insurance helps protect them from potentially costly lawsuits that may result from workplace injuries or illnesses.

It also incentivizes employers to prioritize workplace safety and reduce the risk of on-the-job injuries, which can ultimately lead to a more productive and profitable workplace. Overall, workers’ comp is an essential component of a healthy and safe work environment.

Brief Overview of Common Workers' Comp Claims

These are some of the most frequent types of workplace injuries and can occur due to slippery floors, poor lighting, or uneven surfaces.

Overexertion can lead to injuries such as sprains, strains, and pulled muscles. These injuries often occur from lifting, pushing, pulling, or carrying heavy objects.

These types of injuries often occur due to repetitive motions or awkward postures. They can affect various parts of the body, including the back, neck, shoulders, and wrists.

These injuries occur due to frequent and repetitive movements, such as typing or using a mouse. They can lead to conditions such as carpal tunnel syndrome.

Workers in certain industries, such as manufacturing or food service, may be at risk of burn injuries due to exposure to hot surfaces, chemicals, or flames.

Workers who use sharp tools or equipment, such as knives or saws, may be at risk of cuts and lacerations.

Unfortunately, some workplaces may be at risk of violence from customers or coworkers, which can lead to injuries such as bruises, cuts, or broken bones.

By taking steps to prevent these types of injuries, employers can help reduce the risk of workers’ comp claims and create a safer workplace for their employees.

Common Workers' Comp Claims

This type of claim occurs when an employee slips or trips on a wet or slippery surface, or on an object left in a walkway. Falls can occur from heights, such as falling from a ladder, or from a lower level, such as falling off a step or down a flight of stairs.

Slips, trips, and falls are one of the most frequent types of workers’ comp claims, accounting for a significant percentage of workplace injuries. These types of injuries can occur in any workplace, from offices and retail stores to construction sites and factories.

Slips occur when a worker loses their footing on a wet or slippery surface, such as a spilled liquid, a freshly mopped floor, or a patch of ice. Trips occur when a worker’s foot catches on an object left in a walkway, such as a cord or a loose rug. Both slips and trips can cause the worker to fall, leading to injuries such as broken bones, sprains, or head injuries.

Falls can occur from a height, such as falling off a ladder or scaffolding, or from a lower level, such as falling down a flight of stairs. Falls from heights can be particularly dangerous, as they can cause severe injuries such as traumatic brain injuries or spinal cord injuries.

Preventing slips, trips, and falls in the workplace requires ongoing efforts from both employers and employees. Employers can take steps to maintain safe walking surfaces, such as promptly cleaning up spills, ensuring that floors are properly maintained, and providing appropriate footwear for workers. They can also mark hazardous areas with warning signs and install handrails and guardrails in areas where falls are more likely.

Employees can also do their part by following safety procedures, reporting any hazards or unsafe conditions, and wearing appropriate footwear for their job. By working together to prevent slips, trips, and falls, employers and employees can create a safer workplace for everyone.

Overexertion injuries occur when an employee strains or pulls a muscle due to lifting, pushing, pulling, or carrying heavy objects. They can also occur from repetitive motions, such as twisting, bending, or reaching.

Overexertion injuries are a common type of workplace injury that can result in significant pain and discomfort for employees. These types of injuries occur when a worker performs a task that exceeds their physical limits, leading to strains, sprains, or other soft tissue injuries.

One of the most common causes of overexertion injuries is lifting heavy objects. When workers lift objects that are too heavy or are lifted improperly, they can strain their muscles, causing pain and discomfort. In addition, pushing or pulling heavy objects can also cause overexertion injuries if workers do not use proper techniques or if the task is too strenuous for their physical capabilities.

Repetitive motions can also lead to overexertion injuries, as they can cause strain on muscles and joints over time. Tasks such as typing, using a mouse, or assembly line work can lead to conditions such as carpal tunnel syndrome or tendonitis.

To prevent overexertion injuries, employers can take steps such as providing lifting equipment or training workers on proper lifting techniques. They can also reduce the risk of repetitive motion injuries by providing ergonomic workstations and allowing for regular breaks to rest and stretch.

Employees can also take steps to prevent overexertion injuries, such as using proper lifting techniques, taking regular breaks, and using ergonomic equipment such as chairs and keyboards. By working together to prevent overexertion injuries, employers and employees can create a safer and healthier workplace.

These types of injuries occur when an employee twists or overextends a muscle or tendon, resulting in a strain or sprain. They can happen due to heavy lifting, awkward postures, or repetitive motions.

Strains and sprains are common types of workplace injuries that can occur when an employee overexerts or twists a muscle or tendon beyond its normal range of motion. These injuries can happen due to a variety of reasons, including heavy lifting, awkward postures, or repetitive motions.

A strain occurs when a muscle or tendon is stretched or torn due to excessive force or overuse. This can result in pain, swelling, and limited mobility. Strains can happen in any part of the body, but are most commonly seen in the back, neck, and shoulders.

A sprain, on the other hand, occurs when a ligament is stretched or torn due to sudden twisting or wrenching movements. This can cause pain, swelling, and bruising around the affected joint, and can make it difficult to move the joint or bear weight on it.

Both strains and sprains can be caused by a range of workplace hazards, including lifting heavy objects without proper technique or assistance, performing repetitive motions without taking breaks, or working in awkward postures that place excessive strain on the muscles and tendons.

Employers can help prevent strains and sprains by providing proper training on safe lifting techniques, ensuring that employees take regular breaks to stretch and rest, and using ergonomic equipment to reduce strain on the body. If a strain or sprain does occur, it is important to seek medical attention promptly to prevent further damage and facilitate a speedy recovery.

Repetitive motion injuries occur due to frequent and repetitive movements, such as typing, using a mouse, or assembly line work. They can lead to conditions such as carpal tunnel syndrome, tendonitis, or bursitis.

Repetitive motion injuries are a common type of workplace injury that can occur due to frequent and repetitive movements. These movements can include typing, using a mouse, or assembly line work, among other activities. Repetitive motion injuries can lead to a range of conditions, including carpal tunnel syndrome, tendonitis, and bursitis.

Carpal tunnel syndrome is a condition that affects the wrist and hand. It is caused by compression of the median nerve, which runs through the carpal tunnel in the wrist. Symptoms of carpal tunnel syndrome can include pain, numbness, tingling, and weakness in the hand and wrist.

Tendonitis is a condition that affects the tendons, which are the connective tissues that attach muscles to bones. It is caused by repetitive motions that put strain on the tendons, leading to inflammation and pain. Tendonitis can occur in any part of the body where tendons are present, but is most commonly seen in the shoulders, elbows, and wrists.

Bursitis is a condition that affects the bursae, which are small fluid-filled sacs that cushion the joints. It is caused by repetitive motions that put pressure on the bursae, leading to inflammation and pain. Bursitis can occur in any joint that has a bursa, but is most commonly seen in the shoulders, hips, and knees.

Employers can help prevent repetitive motion injuries by providing ergonomic equipment, such as adjustable chairs and keyboards, and by implementing job rotation and break schedules to reduce the amount of time employees spend performing repetitive tasks. Additionally, employees can take steps to prevent these injuries by using proper technique, taking breaks to stretch and rest, and seeking medical attention promptly if symptoms arise.

Burns can occur from exposure to hot surfaces, chemicals, or flames. Workers in certain industries, such as manufacturing or food service, may be at greater risk of burn injuries.

Burns are a type of workplace injury that can occur from exposure to hot surfaces, chemicals, or flames. Burns can range from mild to severe, and can cause significant pain, scarring, and even death in severe cases. Workers in certain industries, such as manufacturing or food service, may be at greater risk of burn injuries.

Burns caused by exposure to hot surfaces or flames can happen in a variety of workplace settings, such as factories, construction sites, and kitchens. These burns can result from contact with hot machinery, steam, or open flames, and can range from first-degree burns (mild burns that only affect the top layer of skin) to third-degree burns (severe burns that damage all layers of skin and underlying tissue). Severe burns can also cause shock, dehydration, and infection, and can require extensive medical treatment and rehabilitation.

Burns caused by exposure to chemicals can occur in industries such as manufacturing, agriculture, and healthcare. These burns can result from contact with strong acids or alkalis, or from chemical splashes or spills. Chemical burns can be especially dangerous, as they can cause tissue damage that may not be immediately visible. These burns can range from mild to severe, and can cause long-term damage to the affected area if not treated promptly and properly.

Employers can help prevent burn injuries by providing proper training on the safe use of machinery and equipment, implementing appropriate safety procedures, and providing personal protective equipment, such as heat-resistant gloves and clothing. Additionally, employees can take steps to prevent burns by following safety procedures, using protective equipment, and reporting any hazards or unsafe conditions to their employer.

If a burn injury does occur, it is important to seek medical attention promptly to prevent further damage and facilitate a speedy recovery. Severe burns may require hospitalization and specialized treatment, such as skin grafts or physical therapy.

Workers who use sharp tools or equipment, such as knives or saws, may be at risk of cuts and lacerations. This type of injury can also occur from broken glass or other sharp objects.

Cuts and lacerations are a common type of workplace injury that can occur when workers use sharp tools or equipment, such as knives or saws. This type of injury can also occur from broken glass or other sharp objects. Workers in industries such as construction, manufacturing, and food service may be at a higher risk of cuts and lacerations.

Cuts and lacerations can range from minor injuries that require basic first aid to severe injuries that may require surgery and extended recovery time. The severity of the injury depends on the depth and location of the cut or laceration, as well as the size and shape of the object that caused the injury.

Workers can help prevent cuts and lacerations by using appropriate safety equipment, such as cut-resistant gloves and safety glasses, when handling sharp tools or equipment. Employers can also help prevent these injuries by providing training on the safe use of tools and equipment, implementing appropriate safety procedures, and ensuring that workers have access to appropriate personal protective equipment.

If a cut or laceration does occur, it is important to seek medical attention promptly to prevent infection and ensure proper healing. Depending on the severity of the injury, treatment may include cleaning and dressing the wound, stitches or staples, and antibiotics to prevent infection. In some cases, surgery may be required to repair damaged tissue and nerves.

Unfortunately, some workplaces may be at risk of violence from customers or coworkers, which can lead to injuries such as bruises, cuts, or broken bones. This can include physical altercations or threats of violence.

Workplace violence refers to any act or threat of physical violence, harassment, intimidation, or other threatening behavior that occurs at the workplace. Workplace violence can result in a range of injuries, from minor bruises and cuts to serious physical harm, including broken bones, internal injuries, or even death.

Violence at work can come from a variety of sources, including customers, clients, coworkers, and even strangers. It can be triggered by various factors, such as stress, frustration, mental illness, substance abuse, personal disputes, or workplace conflicts.

Physical altercations are one form of workplace violence, which may include punching, kicking, hitting, or pushing. Such acts can cause serious injuries, and can be particularly dangerous if they occur in hazardous work environments, such as construction sites or factories. Moreover, verbal threats of violence, intimidation, or harassment can also cause significant harm, such as emotional distress or anxiety.

Employers have a legal responsibility to provide a safe working environment for their employees, which includes taking appropriate measures to prevent and address workplace violence. This may involve implementing policies and procedures to prevent violence, such as training programs for employees, security measures, and incident reporting protocols.

In conclusion, workplace violence can have serious physical and emotional consequences for victims, and can disrupt the workplace as a whole. It is essential for employers to take steps to prevent and address workplace violence, to ensure the safety and well-being of their employees.

By identifying the most frequent types of workers’ comp claims and understanding how they occur, employers can take steps to prevent these injuries from happening in the first place.

How to Avoid Common Workers' Comp Claims

Tips for employers on how to prevent workplace injuries, such as:

~ Maintaining a clean and organized workspace

~ Providing proper training and education to employees

~ Offering ergonomic equipment and workstations

~ Encouraging employees to take breaks and stretch regularly

What to Do if an Injury Occurs

Explanation of the steps employees should take if they are injured on the job, including:

~ Reporting the injury to their supervisor as soon as possible

~ Seeking medical attention

~ Filing a workers’ comp claim

Preventing common workers’ comp claims is crucial for both the well-being of employees and the financial health of the company. By implementing safety protocols, providing training, and fostering a culture of safety, employers can reduce the risk of workplace injuries and save money on workers’ compensation insurance premiums.

Employers who prioritize workplace safety demonstrate their commitment to the well-being of their employees, and create a positive work environment that promotes productivity, loyalty, and job satisfaction. By investing in injury prevention measures, employers can protect their workforce and promote long-term success for their business.

In conclusion, it is essential for employers to prioritize workplace safety and injury prevention. By taking proactive steps to reduce the risk of workplace injuries, employers can create a safer, healthier, and more productive workplace for their employees.

What is The Difference Between Workers Comp and Disability?

Hello everyone, today we’re going to talk about a topic that’s very important to all of us – the difference between workers’ compensation and disability benefits.

What is Workers' Compensation?

Firstly, let’s start with workers’ compensation. This is a type of insurance that employers are required to carry in order to provide benefits to employees who are injured or become ill as a result of their job. Workers’ compensation can cover things like medical expenses, lost wages, and even rehabilitation costs.

As someone who has worked in a variety of industries throughout my life, I understand just how important it is to have access to these types of benefits when something unexpected happens.

What are Disability Benefits?

On the other hand, disability benefits are designed to provide financial assistance to individuals who are unable to work due to a physical or mental disability, regardless of whether the disability was caused by their job.

Disability benefits can be provided through government programs, such as Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI), or through private insurance policies.

So, the main difference between workers’ compensation and disability benefits is that workers’ compensation is specifically for employees who are injured or become ill as a result of their job, while disability benefits are more broadly available to individuals who are unable to work due to a disability.

Four Benefits of Workers Compensation

Workers’ compensation is a legally mandated insurance program that provides benefits to employees who sustain injuries or illnesses during the course of their employment. Here are four benefits of workers’ compensation:

Workers' compensation provides financial support to employees who are unable to work due to their job-related injuries or illnesses. It covers medical expenses, lost wages, and rehabilitation costs, which can help alleviate the financial burden of work-related injuries.

Employers who carry workers' compensation insurance are incentivized to maintain a safe working environment. By implementing safety measures and reducing workplace hazards, employers can reduce the number of work-related injuries and illnesses, which in turn can lower the cost of insurance premiums.

Workers' compensation insurance provides a no-fault system, meaning that employees do not have to prove that their employer was at fault for their injury or illness. This eliminates the need for legal battles and settlements, which can be time-consuming and costly for both parties.

By providing workers' compensation benefits, employers show their commitment to the health and well-being of their employees. This can improve employee morale and loyalty, leading to increased productivity and a more positive work environment.

Four Benefits of Benefits of Disability:

Disability benefits are a form of financial assistance provided to individuals who have a physical or mental disability that prevents them from working. Here are four benefits of disability benefits:

Disability benefits provide financial support to individuals who are unable to work due to their disability. This support can include monthly payments, medical care, and other essential services that help disabled individuals meet their basic needs.

Disability benefits can help alleviate the financial burden on families of disabled individuals who may be unable to work and earn a living. This can provide peace of mind and stability for families who may be struggling to make ends meet.

Disability benefits may provide access to healthcare services that may not be affordable or available to disabled individuals. This can include medical treatment, prescription medications, and rehabilitation services that can help improve the quality of life for disabled individuals.

Disability benefits can provide disabled individuals with the financial resources they need to live independently and achieve a greater level of self-sufficiency. This can include support for education and vocational training programs that can help disabled individuals re-enter the workforce and improve their earning potential over time.

Whether you’re a construction worker who falls off a ladder or an office employee who develops a chronic illness, knowing the difference between workers’ comp and disability benefits can make all the difference in the world.

It’s important to note that navigating the world of workers’ compensation and disability benefits can be complex and confusing. If you have questions or need assistance, it’s always a good idea to consult with an experienced attorney or other qualified professional.

An attorney or other qualified professional can help you understand the eligibility requirements, application process, and potential benefits available under each program.

They can also help you navigate any legal disputes that may arise and ensure that you receive the maximum amount of benefits to which you are entitled.

In addition to legal assistance, there are other resources available to help individuals understand their rights and options when it comes to workers’ compensation and disability benefits. These may include government agencies, nonprofit organizations, and advocacy groups that provide information, education, and support to individuals with disabilities.

Ultimately, whether you’re dealing with a work-related injury or a disabling condition, it’s important to know your rights and seek the help you need to navigate the system. With the right guidance and support, you can access the benefits and resources you need to get back on your feet and move forward with your life.

That’s it for today, folks. Remember, stay informed and stay empowered!

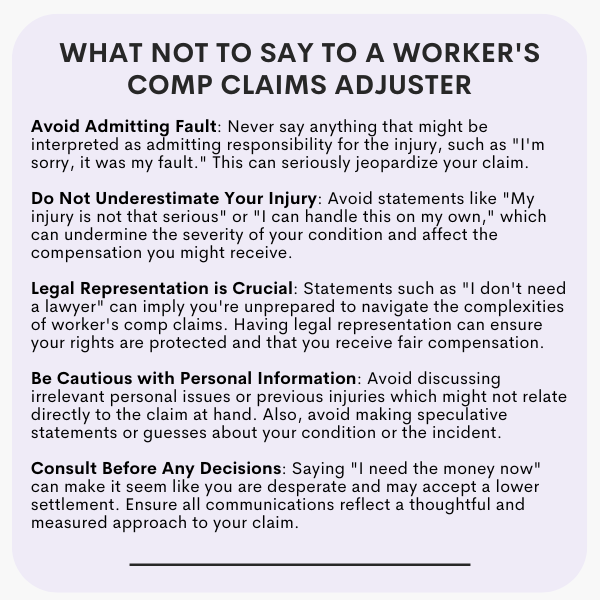

Nine Things You Should Avoid Saying to Your Worker’s Comp Adjuster

When you get injured at work, filing a worker’s comp claim can be a daunting task. The claims adjuster may ask you seemingly innocuous questions that could hurt your case later on.

Knowing what NOT to say is crucial to ensure that you receive the compensation you deserve.

In this blog post, we will go through the top nine things that you should avoid saying when dealing with a worker’s comp claims adjuster. From “I don’t need a lawyer” to “I need the money now,” we will cover all the red flags that could potentially ruin your case. It’s important to be careful of what you say and how you say it because every word counts when it comes to worker’s comp claims.

Read on to know why it is essential to know what not to say when dealing with a worker’s comp claims adjuster.

When it comes to worker’s compensation claims, communication is key. Saying the wrong things can be detrimental to both parties involved – the injured employee and the employer.

It’s important to avoid statements that could be interpreted as admitting fault or downplaying injuries. Making insensitive comments to an injured employee can also lead to negative consequences for both parties. It’s crucial to follow proper protocols and procedures when handling worker’s compensation claims.

Approaching conversations with empathy and understanding is crucial while still protecting the business interests.

The goal should always be to find a solution that benefits everyone involved. Effective communication can go a long way in achieving this goal, and avoiding certain phrases or words can help make the process smoother for all parties involved.

Importance of Knowing What Not to Say to a Workers' Comp Claims Adjuster

When you are filing a workers’ compensation claim, it’s imperative to know what not to say to the claims adjuster. These adjusters are trained to scrutinize claims and look for ways to reduce or deny compensation. Saying the wrong thing can undermine your chances of receiving fair compensation for your injuries.

To effectively communicate with the adjuster, it’s crucial to avoid admitting fault or downplaying the severity of your injuries. Instead, focus on providing only necessary information and sticking to the facts.

Knowing what not to say can make a significant difference in the outcome of your claim and ensure that you receive the appropriate compensation for any workplace injuries you have suffered.

Top Nine Things NOT to Say to Your Worker's Comp

It’s important to be cautious and mindful of what you say when dealing with worker’s comp. Avoid admitting fault or taking responsibility for the injury as it may affect your claims. It is crucial not to exaggerate or downplay the severity of the injury, as this may also impact your claims. Making statements that contradict medical reports or other evidence should be avoided.

It’s best not to discuss unrelated personal issues with the worker’s comp representative, and refrain from discussing settlement offers without consulting a lawyer. Negative comments about your employer or coworkers should be avoided. Additionally, making assumptions about workers’ comp laws and regulations can lead to misunderstandings.

It is advisable not to discuss previous injuries or worker’s comp claims that you may have filed. Lastly, the injury should not be discussed with anyone other than your employer and designated worker’s comp representatives. Do not sign any paperwork without fully understanding its contents, and consult with a lawyer if necessary.

When it comes to communicating with your worker's compensation provider, it's important to avoid saying anything that could be interpreted as admitting fault.

Statements like “I’m sorry, it was my fault” can harm your chances of receiving benefits. Instead, stick to the facts of the incident and avoid offering unnecessary commentary.

It’s important to provide accurate details about what happened and let the insurance adjuster investigate the incident further. Even if you feel responsible for the accident, there may be other factors at play that could impact your eligibility for worker’s compensation. So, it’s best to avoid making statements that could be interpreted as admitting guilt or negligence.

By providing factual information and avoiding speculation or apology, you can help ensure that your worker’s compensation claim is handled fairly and efficiently.

When it comes to filing a worker's compensation claim, it's always advisable to seek legal advice. A lawyer can help you understand your rights and responsibilities under the law, and ensure that you receive the compensation you deserve.

Avoid saying “I don’t need a lawyer,” as this may imply that you are willing to accept whatever settlement is offered, even if it’s not fair. Keep in mind that insurance companies have lawyers working for them, and having your own legal representation can level the playing field. Don’t hesitate to seek the advice of a qualified attorney before filing your worker’s comp claim.

While it may be tempting to try and handle your worker's compensation claim on your own, doing so can lead to mistakes and potentially result in loss of benefits.

Seeking legal advice and guidance from an experienced attorney is crucial when dealing with a worker’s comp claim. An attorney can help you navigate the complex legal system, ensure that you receive fair compensation, and protect your rights.

Saying “I’ll take care of this on my own” can be seen as a sign of negligence or lack of interest in your claim. It’s important to recognize the value of professional help when dealing with a potentially life-altering situation. By seeking the assistance of an attorney, you increase your chances of a successful outcome and avoid any unnecessary setbacks.

Remember that your health and well-being are at stake, so it’s crucial to prioritize getting the support you need to ensure proper compensation for your injuries.

After a workplace injury, it is crucial to seek medical attention as soon as possible. Delaying treatment can worsen your injury and may harm your chances of receiving worker's comp benefits.

When filing a claim, telling your employer or insurance company that you haven’t seen a doctor could be used against you. It is important to document any injuries and medical treatment received to support your claim.

If you are unsure about what to say to your worker’s comp, it may be helpful to consult with an experienced attorney. They can provide guidance on how to navigate the claims process and protect your rights as an injured worker.

Remember, seeking timely medical attention and proper documentation are key steps in ensuring that you receive the compensation you deserve.

When filing a worker's compensation claim, it's crucial to provide accurate and detailed information. One common mistake is saying "I can't remember all the details".

If you find yourself struggling to recall certain aspects of the incident, take some time to review your notes or speak with witnesses before submitting your claim. Avoid making guesses or assumptions about what happened, as this can lead to inconsistencies in your story.

It’s also essential to be honest about any pre-existing conditions or injuries that may have contributed to the incident. Remember that any false statements made during the claims process could result in serious consequences. By taking the time to gather all relevant information and providing it truthfully, you increase your chances of a successful worker’s compensation claim.

When it comes to dealing with worker's compensation, it's important to be truthful and accurate about the extent of your injury.

One common mistake people make is downplaying their injury by saying “my injury is not that serious.” This can harm your chances of receiving proper compensation, as even minor injuries can have long-term effects and require medical attention.

To ensure you receive the compensation you deserve, it’s crucial to accurately describe the extent of your injury and how it affects your ability to work. Be honest about any pain or limitations you are experiencing, and document the severity of your injury through medical records and other evidence. By doing so, you’ll be in a better position to receive fair compensation for your workplace injury.

If you have a pre-existing condition and are filing for workers' compensation, it's important to be careful about what you say to your representative.

While it can be tempting to disclose this information, doing so can actually harm your claim. However, it’s important to remember that having a pre-existing condition does not automatically disqualify you from receiving workers’ compensation benefits.

Instead of focusing on your pre-existing condition, try to provide detailed information about your work-related injury. Be honest and transparent with your workers’ comp representative about the circumstances surrounding your injury, but avoid providing unnecessary or irrelevant information.

Remember that workers’ comp is designed to protect you and help you recover from work-related injuries, so providing accurate and relevant details is key in getting the support you need.

When filing a workers' compensation claim, it's important to be truthful about the circumstances surrounding your injury.

One common mistake is claiming an injury that occurred outside of work. If you weren’t injured on the job, then your workers’ compensation claim may not be valid and can result in fraud charges and legal consequences.

It’s understandable to feel pressure when it comes to filing for workers’ comp, but honesty is always the best policy. If you’re unsure whether your injury qualifies for workers’ compensation, consult with a qualified attorney or medical professional.

Being transparent about your injury will help to avoid any complications or repercussions down the line. Remember, attempting to deceive or mislead your employer or insurance provider can have serious consequences.

When filing a worker's compensation claim, it's important to avoid making statements that could harm your case.

One common mistake is asking for immediate payment, which can make it appear as though you are only interested in the money and not your recovery. Instead, prioritize your healing process and follow the proper procedures for filing a claim.

It’s also important to avoid making any statements that could be interpreted as admitting fault or downplaying the severity of your injury. Be honest and accurate in describing the accident and your injuries to avoid any discrepancies in your claim.

Working with a qualified attorney who specializes in worker’s compensation can help you navigate the process and avoid common mistakes. By following these guidelines and working with an experienced professional, you can increase your chances of receiving fair compensation for your injuries.

If you've been injured on the job, it's important to file a worker's compensation claim even if you don't feel like it's necessary.

Saying “I don’t want to file a claim” can prevent you from receiving the compensation you need for medical bills and lost wages. It’s crucial to report all injuries, no matter how minor they may seem at the time. Waiting too long to report an injury can make it more difficult to prove that it happened on the job.

To ensure that you receive proper treatment and compensation, be honest with your employer and doctor about the details of your injury. Worker’s compensation is designed to protect both employers and employees in case of workplace accidents or injuries, so it’s important to take advantage of this resource when needed.

Remember, filing a claim doesn’t just protect you – it also helps ensure that workplace safety standards are upheld for everyone.

Importance of Being Careful of What You Say to a Claims Adjuster

When dealing with a worker’s compensation claim, it’s crucial to be mindful of what you say to the claims adjuster. It’s important to remember that they are not your friend and may use anything you say against you. To avoid any potential issues, it’s best to stick to the facts and avoid making any statements that could be construed as admitting fault for the injury or accident.

Additionally, it’s important not to make assumptions about the outcome of your claim or reveal any confidential information. Exaggerating your injuries or downplaying their severity can also work against you. Instead, focus on providing accurate information and avoiding emotional or defensive responses during conversations with the claims adjuster.

By being careful about what you say, you can help ensure a fair and just outcome for your worker’s compensation claim.

In conclusion, a workers’ compensation claim is a legal process that requires careful consideration of every word spoken to the claims adjuster.

You must always be mindful of what you say and how you say it. Avoid saying things like “I’m sorry, it was my fault,” or “I don’t need a lawyer.” Instead, always speak the truth and provide accurate information about your injury. It’s important to remember that anything you say can be used against you in court, so it’s better to stay quiet if you’re not sure what to say.

To learn more about what not to say to your workers’ comp claims adjuster, read our comprehensive guide on the top nine things NOT to say.

Workers vs Workmans Comp: What You Need To Know

Are you confused about the difference between Workman’s and Workers’ Compensation? Are you aware of your rights as an employee if you get injured on the job? If not, don’t worry! We’re here to help.

In this blog, we will be focusing on Florida state laws and how they apply to workers’ compensation. We will discuss what workers’ compensation is, its importance, and how it differs from Workman’s Compensation.

Additionally, we’ll cover the types of benefits available for injured workers in Florida, eligibility criteria, common exemptions, and how to file a claim. Finally, we’ll also answer some frequently asked questions and provide tips on choosing the right lawyer in case you need one.

Understanding Workers’ Compensation in Florida

Workers’ compensation is a type of insurance that provides benefits to employees who suffer work-related injuries or illnesses. In Florida, it’s mandatory for employers to have workers’ compensation insurance.

It provides medical expenses coverage, lost wages, and disability benefits to eligible employees. However, the process of filing a workers’ compensation claim can be complex, especially when there are disputes between the employee and employer. Hence, in such cases, hiring an attorney experienced in workers’ compensation cases would be a wise decision.

It is also essential for both employers and employees to understand their rights and responsibilities related to workers’ compensation in Florida. Employers must ensure that their employees receive proper safety training and provide them with a safe work environment to avoid accidents.

Employees should report any injuries or illnesses sustained at work immediately to their employer or supervisor, as failing to do so could result in the loss of benefits under the workers’ compensation system.

What is Workers’ Compensation and Why is it Important?

Workers’ compensation is a form of insurance that provides benefits to employees who become injured or ill while on the job. These benefits include coverage for medical expenses, lost wages, and rehabilitation costs. In the event of a work-related death, workers’ compensation also provides death benefits to the family of the employee.

It’s crucial for employers to have workers’ compensation insurance as it not only protects their employees but also the business itself.

By having this coverage, employees can feel secure in the knowledge that they will receive assistance in case of an accident or illness at work.

However, it’s important to note that workers’ compensation laws can vary by state, so it’s essential to understand the specific regulations in your area to ensure compliance with local laws and protect both employees and the business.

How is Workers’ Compensation Different from Workman's Compensation?

When it comes to understanding the system that provides benefits to employees who are injured or become ill due to their job, it’s important to differentiate between Workers’ Compensation and Workman’s Compensation.

While the two terms are often used interchangeably, they refer to the same thing and the exact terminology varies by state. In Florida, this system is referred to as workers’ compensation.

Under workers’ compensation, eligible employees can receive benefits that cover medical expenses, lost wages, and disability payments.

The system exists to protect employees in case of work-related injuries or illnesses. Employers are required by law to carry workers’ compensation insurance as a way of safeguarding their employees.

Overall, whether you refer to it as Workers’ Compensation or Workman’s Compensation, the important thing is understanding how the system works and what benefits it offers.

Florida Workers’ Comp Benefits

If an employee in Florida suffers a work-related injury or illness, they may be eligible for benefits under the workers’ comp system. These benefits can include medical treatment, lost wages, and vocational rehabilitation services to help them get back on their feet.

Employers in Florida are required to carry workers’ comp insurance to protect both their employees and business from legal consequences.

Workers’ comp covers a wide range of injuries, including physical injuries and mental health conditions. Employees should report any work-related injury or illness as soon as possible so they can begin the process of receiving benefits.

Types of Benefits Available for Injured Workers

If you have been injured on the job in Florida, it’s important to understand your rights and options under Florida Workers’ Comp. This program provides various benefits to injured workers, including medical benefits, wage replacement benefits, and death benefits.

Medical benefits cover the cost of necessary medical treatment for work-related injuries or illnesses. This can include everything from doctor visits to surgeries and physical therapy. Wage replacement benefits provide compensation for lost wages due to time off work as a result of the injury. These benefits can help you pay your bills while you recover.

In cases where an injury results in death, Florida Workers’ Comp offers death benefits to dependents of the affected individual.

These benefits can help support loved ones left behind during a difficult time. Understanding the types of benefits available is essential to ensure that you receive the maximum support possible when facing a work-related injury or illness.

How to File a Workers' Comp Claim in Florida

Workers’ compensation is an insurance program that offers benefits to employees who get injured while carrying out their job duties.

In the state of Florida, workers’ comp benefits may comprise medical expenses, lost wages, and rehabilitation costs.

If you have been injured while working, it’s essential to report your injury to your employer within 30 days of the incident. Your employer must then report your injury to their insurance carrier within seven days.

Filing a workers’ comp claim in Florida necessitates following all necessary measures and deadlines to ensure that you receive the benefits you deserve. It’s crucial to follow the correct procedures and provide all relevant information as soon as possible to expedite the claims process.

This will help ensure that you receive timely and adequate compensation for any work-related injuries or illnesses.

Eligibility for Workers’ Compensation in Florida

Workers’ Compensation is a state-mandated insurance program that offers benefits to employees who suffer an injury or illness in the course of their job.

In Florida, most employers are required by law to provide Workers’ Compensation coverage to their employees. An employee is eligible for Workers’ Compensation benefits in Florida only if the injury or sickness occurred while they were performing work-related duties.

To be eligible for benefits, workers must notify their employer of their injury or illness within 30 days and seek medical attention from an authorized medical provider. It is essential to follow these regulations to receive your due Workers’ Compensation benefits in Florida.

In the state of Florida, workers who suffer an injury or illness due to their job may be eligible for workers’ compensation.

This includes both full-time and part-time employees, as well as independent contractors in certain situations.

To qualify for benefits, workers must have suffered an injury or illness that is related to their job duties or workplace environment. However, there are some exceptions to this rule, such as injuries caused by an employee’s own intentional misconduct or drug/alcohol abuse.

To ensure that they receive the benefits they are entitled to, it is important for workers to promptly report any workplace injuries or illnesses to their employer. By doing so, they can take advantage of the protections offered by workers’ compensation laws in Florida.

In Florida, most employers are required to provide workers’ compensation insurance, but there are some exemptions to this requirement.

Certain types of employees, including independent contractors and domestic workers, may not be eligible for workers’ comp coverage. Additionally, employers with fewer than four employees are exempt from providing workers’ compensation insurance.

Exceptions may also apply to certain industries or occupations such as agricultural workers or temporary employees. It’s important to understand your eligibility for workers’ compensation in Florida and any possible exemptions that may apply.

Knowing your rights and responsibilities can help ensure that you are protected in case of a workplace injury or illness.

How to Get Help with Your Workers’ Comp Claim in Florida

If you have been injured on the job, it’s important to understand the difference between Workman’s and Workers’ Comp before filing a claim in Florida. Seeking legal assistance from an experienced Workers’ Comp attorney is highly recommended.

The first step is to report the injury to your employer immediately, and seek medical attention. It’s essential to keep track of all medical treatment, expenses, and missed work due to the injury.

Effective communication with your employer and their insurance company throughout the claims process is crucial. By following these steps and seeking legal guidance, you can get help with your Workers’ Comp claim in Florida and receive fair compensation for your injuries.

When it comes to getting help with your workers’ compensation claim in Florida, there are several factors to consider. If your employer denies your claim or offers inadequate benefits, it may be time to contact a workers’ compensation lawyer.

A lawyer can help you navigate the complex legal process and ensure that you receive the compensation you deserve.

There are other situations where contacting a lawyer may be necessary, such as if your injury is severe and requires long-term medical treatment or if you have been discriminated against for filing a claim.

It’s important to act quickly because there are strict deadlines for filing workers’ compensation claims in Florida.

Having a lawyer on your side can provide valuable guidance and support throughout the entire process. They can help you understand your rights and options, negotiate with insurance companies, and represent you in court if necessary.

If you’re unsure whether or not you need a lawyer, it’s always best to consult with one to ensure that your rights are protected.

Tips for Choosing the Right Workers' Comp Lawyer in Florida

If you’re filing a workers’ comp claim in Florida, choosing the right lawyer is crucial to ensuring you receive the benefits you deserve.

A good place to start is by looking for a lawyer with experience in handling workers’ comp cases in Florida. Additionally, it’s important to consider the lawyer’s communication skills and availability to ensure they will keep you updated on your case.

You may also want to check their track record of success in obtaining fair compensation for their clients. Most importantly, make sure the lawyer has a clear understanding of your specific case and is dedicated to fighting for your rights. By following these tips and hiring an experienced and dedicated workers’ comp attorney, you can increase your chances of receiving the compensation you need to cover medical bills, lost wages, and other costs related to your work-related injury or illness.

Frequently Asked Questions about Workers’ Comp in Florida

If you live in Florida and are curious about worker’s compensation insurance, here are some commonly asked questions that may help.

Workers’ comp is insurance designed to provide benefits to employees who suffer an injury or illness on the job. It covers medical expenses, lost wages, and rehabilitation costs. In Florida, most employers are required by law to provide workers’ compensation insurance coverage for their employees.

If you are injured on the job, you should report it immediately to your supervisor or employer as soon as possible. Then, seek medical attention promptly.

Your employer will then file a claim with their insurance company and inform you about your rights and benefits under workers’ compensation.

In Florida, workers’ compensation benefits are calculated based on the severity of the injury and how much time you need off work to recover fully.

However, it is not possible to sue an employer for workplace injuries in Florida due to a no-fault system that offers protection for both employees and their employers.

If you are a business owner in Florida, you may be wondering how much workers’ comp insurance will cost you.

The cost of workers’ comp insurance can vary depending on factors such as the size of your business and the level of risk associated with your industry. Employers in Florida are required to purchase workers’ comp insurance to provide coverage for their employees in case of work-related injuries or illnesses.

The cost of workers’ comp insurance is typically calculated as a percentage of the employee’s payroll. Florida law also requires that all employers who have four or more employees must carry workers’ comp insurance.

If you are unsure about the costs associated with workers’ comp insurance, it’s important to consult with an experienced insurance agent. They can help you understand the different options available and find the best policy for your business at an affordable price.

If you have had a workers’ comp claim denied in Florida, it’s important to understand your legal options. You have the right to file an appeal and request a hearing with a judge. During the hearing, you will need to present evidence to support your claim and explain why you believe it was wrongfully denied.

It may be helpful to hire an experienced attorney who specializes in workers’ comp cases to represent you during the hearing. An attorney can help you prepare and present your case effectively so that you have the best possible chance of winning.

If you still disagree with the decision after the hearing, you can further appeal to a higher court. However, it’s important to note that this process can be time-consuming and expensive, so it’s best to work closely with your attorney throughout the entire process.

If you live in Florida and have been injured at work, you may be wondering if you can sue your employer. Generally speaking, workers’ compensation laws prevent employees from suing their employers for work-related injuries. However, there are some exceptions to this rule. For example, if your injury was caused by intentional harm or gross negligence on the part of your employer, you may be able to pursue legal action.

If you believe that your employer’s actions caused your injury, it is important to speak with an experienced workers’ compensation attorney who can advise you on your legal options. Workers’ compensation benefits may include medical expenses, lost wages, and disability payments.

It is important to report any work-related injuries to your employer as soon as possible in order to preserve your right to workers’ compensation benefits. This will also help ensure that you receive the appropriate medical treatment for your injuries.

In Florida, Workers’ Compensation is a form of insurance that provides medical benefits and wage replacement to employees who suffer from job-related injuries or illnesses.

The term “Workman’s Compensation” is an outdated term and has been replaced by Workers’ Compensation. It is important to understand the differences between these two terms to avoid any confusion in legal matters.

If you have been injured on the job, it is important to know your rights and take action as soon as possible. Contact a workers’ compensation lawyer today for a free consultation to discuss your case and learn about your legal options. Don’t wait, get the help you need today!

Maximizing Workers Comp Benefits for Carpentry Companies

A Comprehensive Guide

Carpentry is a profession that involves a lot of physical labor and often comes with an increased risk of injuries.

As a carpenter, it is essential to have adequate insurance coverage to protect your employees and business in case of any unforeseen circumstances. This comprehensive guide will take you through everything you need to know about maximizing workers’ comp benefits for carpentry companies.

We will cover topics like understanding workers’ comp insurance, the benefits it provides, choosing the right policy for your business, and tips for maximizing benefits.

Additionally, we will also touch upon other types of insurance coverage that could be beneficial for carpentry businesses like general liability insurance, commercial property insurance, etc.

Keep reading to find out how you can ensure the safety and wellbeing of your employees while also protecting your business interests.

Understanding Workers' Comp Insurance For Carpenters

For carpentry companies, workers’ comp insurance is mandatory in almost all states. Given the nature of the work, carpenters face a higher risk of work-related injuries.

In case of an injury or illness, workers’ compensation insurance covers medical expenses, lost wages, and rehabilitation costs. Employers can take steps to reduce the risk of workplace injuries to keep workers’ comp premiums low.

It is essential for carpentry companies to understand their rights and responsibilities under workers’ comp insurance and the claims process to maximize benefits for their employees. By doing so, they can ensure that their employees receive proper care and support in case of a work-related injury or illness.

Benefits of Workers' Comp Insurance for Carpenters

Workers’ compensation insurance provides medical and wage replacement benefits to employees who are injured on the job.

It is particularly important for carpentry companies, as it protects them from costly lawsuits related to workplace injuries. Workers’ comp insurance can also provide vocational rehabilitation services to help injured employees return to work. By prioritizing workplace safety, carpentry companies can reduce the risk of workplace injuries and lower their workers’ comp insurance premiums.

Working with an experienced insurance provider can help maximize their workers’ comp benefits and ensure that employees are protected in case of an accident. Overall, workers’ comp insurance is essential not only for the protection of employees but also for the financial stability and reputation of carpentry companies.

Wage Replacement

Workers’ comp insurance provides important benefits for carpenters who are unable to work due to a job-related injury or illness.

One of the key benefits is wage replacement, which typically covers a portion of the employee’s pre-injury wages. Carpentry companies can choose from different types of wage replacement benefits, such as temporary total disability, permanent partial disability, and permanent total disability, depending on the severity and duration of the injury.

It’s essential for carpentry companies to understand the requirements and limitations of their state’s workers’ comp laws regarding wage replacement benefits.

Maximizing workers’ comp benefits can help carpentry companies support their injured employees while minimizing financial losses. By providing adequate wage replacement benefits, carpentry companies can ensure that their employees have the necessary financial support during their recovery period, allowing them to return to work as soon as possible.

Medical Coverage

One of the key benefits of having workers’ comp insurance for carpenters is the medical coverage it provides. In the event that an employee is injured on the job, workers’ comp insurance can cover a range of medical expenses, including doctor’s visits, hospital stays, surgeries, and rehabilitation services. Additionally, prescription medications and medical equipment can also be covered under this type of insurance.

Employers can choose to offer additional medical coverage options to their employees through their workers’ comp policy, providing even greater protection for their staff. By ensuring that their workers have access to comprehensive medical coverage in the event of an injury, employers can help mitigate potential financial risks while also fulfilling their duty to care for their employees’ wellbeing.

Overall, maximizing workers’ comp benefits by including robust medical coverage is a smart choice for both employers and employees in the carpentry industry.

Disability Benefits

Workers’ comp insurance can provide numerous benefits for carpentry workers, including disability benefits in case of a work-related injury or illness. Disability benefits can provide financial support to cover lost wages while the worker recovers and returns to work. If the injury or illness results in long-term or permanent disability, permanent disability benefits may be available.

Having proper workers’ comp insurance in place is essential for carpentry companies to ensure their employees are protected in case of an accident or injury on the job. It not only provides financial support for injured workers but also protects the company from potential legal and financial liabilities. With these benefits, having workers’ comp insurance is a crucial aspect of any carpentry business plan.

How to Choose the Right Workers' Comp Insurance for Your Carpentry Business

Choosing the right workers’ comp insurance for your carpentry business can be a challenging task. It is crucial to select an insurance provider that has experience in the carpentry industry and understands your specific needs. When selecting a policy, consider the coverage limits and exclusions of the policy, as these can significantly impact the protection you receive. Also, evaluate the provider’s claims process and customer service to ensure timely resolution of claims.

Additionally, look for any additional services offered by providers, such as safety training or risk management consulting that can help reduce workplace injuries. Finally, compare quotes from multiple providers to ensure that you’re getting the best value for your money.

A comprehensive guide on maximizing worker’s comp benefits for carpentry companies will provide insights into all these factors and help you make an informed decision while choosing worker’s comp insurance for your carpentry business.

When choosing the right workers’ comp insurance for your carpentry business, it’s important to compare policies and quotes. This involves considering many factors such as coverage limits, deductibles, and reputation of the insurance provider. Comprehensive coverage for both medical expenses and lost wages is critical, especially in the event of a serious injury or accident.

It’s essential to review your policy regularly to ensure it continues to meet the needs of your carpentry business. Sometimes cheaper policies may not provide adequate coverage when you need it most. Therefore, carefully evaluating different policies and assessing which one is right for you can make all the difference in maximizing workers’ comp benefits for your company.

Choosing the right workers’ comp insurance for your carpentry business requires assessing your specific needs.

This includes considering factors such as the size of your business, the number of employees you have, and the type of work they do. It’s important to choose a policy that covers all potential risks and hazards unique to your industry. You should also look for a policy with adequate coverage limits and benefits that meet both your needs as an employer and those of your employees.

To find the best value for your business, it’s recommended to compare quotes from multiple providers. By taking these steps to assess your needs and compare policies, you can ensure that you are maximizing workers’ comp benefits for your carpentry company while also protecting yourself and your employees in case of accidents or injuries.

When it comes to choosing the right workers’ compensation insurance for your carpentry business, working with an insurance agent can be a valuable resource. An experienced agent can help you navigate the complexities of different policies and coverage options, as well as provide advice on how to minimize risks and reduce premiums.

It’s important to choose an insurance agent who has experience working with carpentry companies and understands the unique risks associated with the industry.

Before hiring an agent, be sure to check their credentials and ask for references. With the right guidance from an insurance agent, you can ensure that your carpentry business is properly protected in case of workplace injuries or accidents.

Tips for Maximizing Workers' Comp Benefits

Maximizing workers’ compensation benefits is crucial for any carpentry company. Encourage your employees to report any work-related injuries promptly to avoid delays in providing them with the necessary treatment. To ensure that you are getting the best possible coverage, work with an insurance provider who has a good understanding of the carpentry industry.

Your company should also develop a return-to-work program that can assist injured employees in getting back to work as soon as possible. Train your employees on safety procedures and provide them with the necessary protective equipment to prevent accidents from occurring.

Keeping detailed records of all workers’ compensation claims and expenses is essential for accurate reporting and analysis. This information can help identify areas where improvements can be made to minimize the risk of future accidents and claims, ultimately reducing costs for your company.

By following these tips, you can maximize workers’ comp benefits and create a safer workplace for everyone involved.

Reporting Injuries and Claims Early

One of the most important tips for maximizing workers’ comp benefits is to report workplace injuries and claims early. Delaying reporting can lead to denial of claims or reduced benefits, so it’s crucial to act promptly. Reporting injuries early not only ensures that workers receive proper medical treatment but also helps them receive compensation for lost wages.

Employers should have clear policies and procedures in place for reporting workplace injuries and workers’ comp claims, and workers should be educated on these policies and encouraged to report any incidents as soon as possible. By promptly reporting injuries and claims, both employers and employees can ensure that they receive the full benefits they are entitled to under workers’ compensation laws.

Providing Quality Medical Care

One effective way to maximize workers’ comp benefits is by providing quality medical care to injured workers. This can help ensure a speedy recovery and minimize the impact of the injury on their ability to work. To achieve this, it’s important to choose a healthcare provider who is experienced in treating work-related injuries and is familiar with the workers’ compensation system.

Additionally, ensuring that your employees receive timely medical treatment and follow-up care, such as physical therapy or rehabilitation if necessary, can also contribute to a successful recovery.

Good communication between the injured worker, the employer, and the healthcare provider can further ensure that everyone is working towards the same goal: getting the worker healthy and back to work as soon as possible. By prioritizing quality medical care for injured workers, carpentry companies can both maximize their workers’ comp benefits and support their valued employees throughout the recovery process.

Accommodating Injured Workers

When it comes to maximizing workers’ comp benefits for carpentry companies, accommodating injured workers is an important aspect to consider. Providing modified duties or job accommodations can help injured workers perform tasks that are within their physical limitations and aid in their recovery and return to work as soon as possible. It’s also crucial for employers to communicate regularly with injured workers, keeping them informed about the status of their claim and any available benefits.